The ROI of Indian Homeownership

Does residential real estate have a place within an intelligent investor's portfolio?

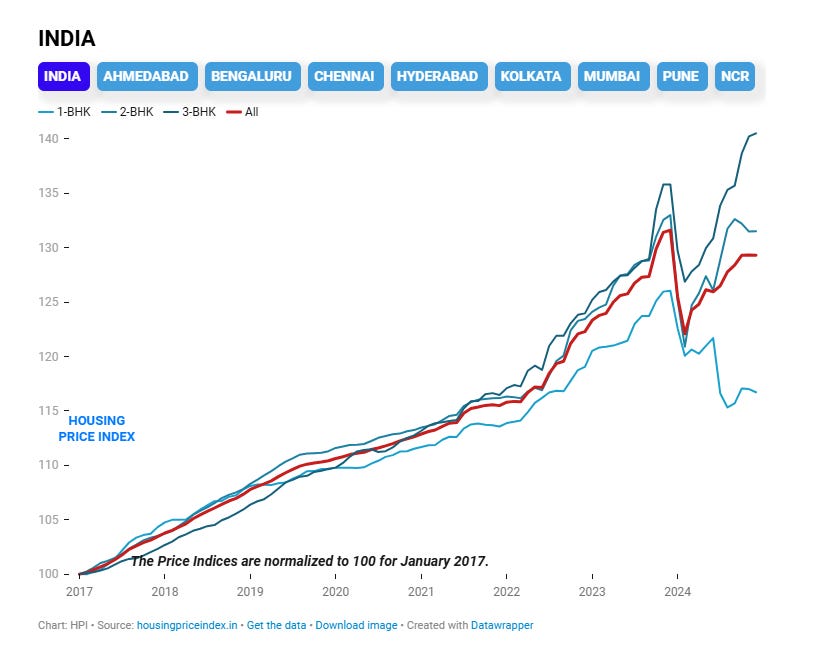

The surge in Indian property values

For many Indians, purchasing a home is the single biggest financial decision they will make in their lives. Historically, it has been a profitable pursuit, with many familiar with stories of 100-fold returns from property acquired in the past few decades.

We Indians also have a strong cultural preference for home ownership, leading to a 86.6% of Indians owning their homes. This has fueled a boom in the Indian real estate market, which has further accelerated since the COVID pandemic. The Indian property price index grew by 31.6% between 2017 and 2024, representing a CAGR of 4%.

art from the property price appreciation, a house also generates a rental income (or imputed rent, if self-occupied) of around 3-5% based on current prices. Adding this to the property price appreciation provides an overall annual return on investment of approximately 7-9%. However, there is no guarantee this return will persist into the future, especially the property price appreciation portion. The current building spree could lead to an over-supply situation a few years down the line, especially if we experience an economic downturn.1

While this may not be as impressive as historical equity returns in India of 15%+, it is considered a far safer investment choice by most Indians. This view is further supported by Indian banks and lenders, who are willing to lend up to 80% of a home's value in the form of a loan. Hence, this has been the preferred investment vehicle for Indians, with Real Estate making up 51% of Indian household assets.

The opportunity cost and IRR of buying a home

Most home buyers, however, overlook the opportunity cost of investment and total return on investment. They often expect the historical 8~9% return in the real estate market to persist or rely solely on "advice" from real estate agents regarding potential returns. To address this, I created an ROI calculator for anyone looking to buy a home: Google sheet link

The model above considers all the major cash inflows and outflows involved in a residential real estate transaction. Key assumptions are listed below - you can modify the sheet to match your own circumstances.

Assumed 5.5% annual inflation until 2040 and 3% for future years; I also used this inflation figure to discount future cash flows

Down-payment of 20% of the property value; Home loan for the remaining 80%, with a interest rate of 8.8% and tenure of 30 years2

Net rental yield of 3%, after factoring in expenses like maintenance, repairs, property taxes, real estate brokerage etc.; Note: this would be lower if you have a low occupancy rate (i.e. many months between tenants)

The estimate does not include a future sale transaction, but rather assumes a perpetual rental income, based on the house remaining tenanted throughout the tenure. While one could argue that the return might be higher due to "property price appreciation", the rental yield more closely estimates the long-term economic value of the house.

Capital gains tax liabilities from previous property sales have not been included (these can be added in row 11 in the sheet)

Based on these assumptions, it would take ~43 years to recover your capital, yielding a 2.8% return on invested capital. This could further deteriorate if you face a large maintenance expenditure or property damage.

Running different scenarios with varying rental yield and loan interest shows that home purchases can, in specific cases, provide adequate returns (shown below). However, based on real estate prices in most major Indian cities, the returns on offer are far lower than those you would get from “risk-free” investments like fixed deposits or government-backed bonds.

In conclusion

“An investment operation is one which, upon thorough analysis, promises safety of principal and an adequate return. Operations not meeting these requirements are speculative.”

Benjamin Graham

Residential real estate, when purchased at appropriate prices, does seem to fit both criteria outlined above: capital preservation and an adequate return.

In a country where rental rates generally keep pace with high inflation, owning a home can be a significant advantage upon retirement, providing a stable living situation without relying solely on income from other sources. However, purchasing a home as a pure investment when rental yields are far lower than prevailing interest rates could lead to sub-par returns.

Thanks for reading and let me know your thoughts!

Sources:

https://www.housingpriceindex.in/

https://www.livemint.com/money/personal-finance/home-loans-top-5-banks-including-hdfc-sbi-icici-bank-kotak-pnb-with-lowest-rates-of-interest-11714133252737.html

A great read on why property prices tend to remain inflated in India regardless of demand: https://www.newslaundry.com/sena/indias-real-estate/

Note: with current loan interest rates being higher than inflation, paying more of the property value upfront provides higher returns

excellent post. I did this mental math while buying my first house in 2022 in Pune. The real estate market was just about to revive (post covid lockdown, a lot of IT folks had gone back to their native places, and the rental market crashed)

My mental math told me that in a steady market, I would be getting a 5-6% rental yield (yes, it was that good due to low housing prices). The home loan rate was 7.25%, so a spread of 1-2% was effectively paying for a 3-4% appreciation yield. 1:2 bet!

I happened on this a few months later than it was first posted. Sorry for the delayed reaction.

In the US, residential mortgage holders benefit from the ability to deduct mortgage interest on their taxes. For rental properties, you can also deduct maintenance costs as well as property taxes, and depreciation on the value of the asset (net of land cost). It's those deductions and the ability to lever up 3:1 (debt : equity) that can turn a property appreciating in low single-digits into something with a 15-20% ROE.

Are none of those tax benefits available to Indian investors in residential real estate?