Nalanda Capital’s “Permanent Portfolio” of India’s best-run companies

The new book by Pulak Prasad, Nalanda Capital’s Founder, is a captivating read for both investors and evolutionary biologists!

What I Learned About Investing from Darwin, is a great book recommendation for anyone interested in value investing, regardless of geography or market. It is jam packed with wisdom from Nalanda Capital’s 16 years of investing in Indian businesses. From 2007 to 2023, the fund generated annualized returns of 20.3% after fees compared to 10.9% for the Indian indices1.

Pulak also draws parallels between the world of investing and evolutionary biology, hypothesizing that the ruthless capitalist system results in the long-term survival of only the fittest businesses.

Nalanda’s investment approach

Avoid big risks

Buy high quality at a fair price

Don’t be lazy - be very lazy

This approach requires them to focus solely on the “best-run” businesses, measured by high returns on capital and prudent management. They are long-term investors, with their favourite holding period being “forever”.

These are the four key elements for a “permanent investment” at Nalanda:

Unlike most other investors, Nalanda relies solely on a company’s historical track record to assess its durable competitive advantage. Return on Capital Employed (ROCE) is their preferred way to identify a company’s competitive advantage. Nalanda’s benchmark of 20%+ historical ROCE requires that their portfolio of companies earns at least ₹20 for every ₹100 invested in their operations. In contrast, listed Indian companies in aggregate earn around 8%~12% ROCE2.

Nalanda is also refreshingly candid about what companies are in their portfolio. A full list of their current holdings can be found here. I’ve visualized the portfolio based on PE, ROCE and market cap below3

A better view of the large cluster on the bottom-left:

As you would expect, companies with higher ROCEs (indicating stronger competitive positions) are assigned a higher PE ratios. The average PE for the Nalanda portfolio is an eye-watering 49.9 , with the median being 34.8. This is far higher than the NIFTY 500 index, which trades at a PE of 24.74. Most of their portfolio companies were bought at sub-20 PE ratios, usually during market downturns like 2008 or 2020.

Nalanda view themselves as “permanent owners” rather than speculative investors in a business. So, as long as the company maintains their market position, Nalanda has committed to never sell. Hence, their motto: “Don’t be lazy, be very lazy”.

“When we find high quality businesses that do not fundamentally alter their character over the long term, we should exploit the inevitable short-term fluctuations in their business for buying and not selling”

Nalanda will only sell a portfolio company for only one of three reasons listed:

A decline in governance standards (none so far)

Egregiously wrong capital allocation (3 exits)

Irreparable damage to the business (6 exits)

So, 9 exits in total over a 16 year period!

That being said, they aren’t complacent. Pulak and the team still routinely track their portfolio companies to gauge whether their original investment thesis remains valid.

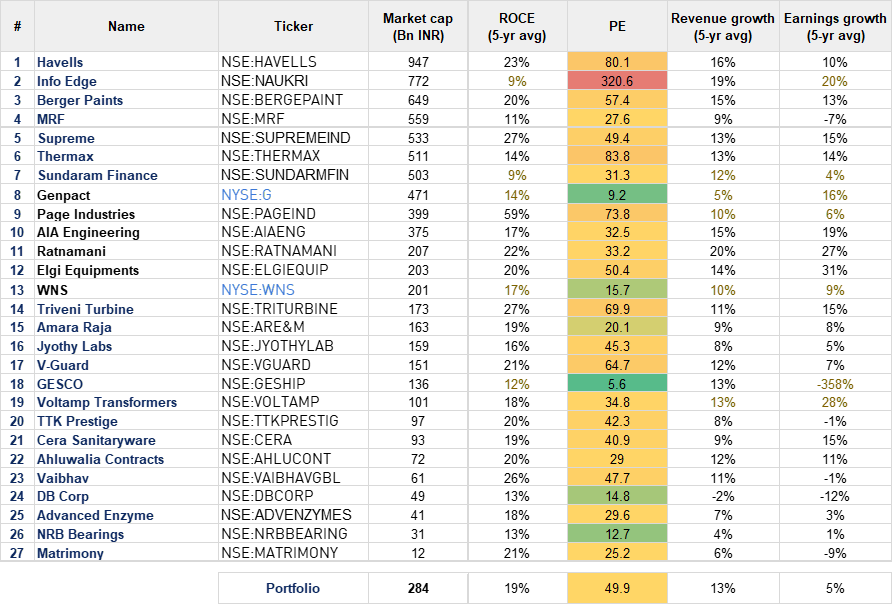

Here is their full list of holdings ranked by market cap:

These 27 businesses seem to be among the best-run in India, making them essential additions to an Indian investor’s watchlist. Apart from current holdings, Pulak also mentions “Asian Paints” as a company that is “sadly not in our portfolio”.

Although most of these seems optically over-valued, there are some which trade at more reasonable multiples and merit a closer look: Amara Raja, GE Shipping, DB Corp, NRB Bearings, Genpact, WNS.

Due to Nalanda’s size, their investment universe comprises of Indian companies that have a market cap greater than $100 million (₹8.4Bn). 800 of the ~5300 listed Indian companies meet this criteria. Out of these, only 10% or ~80 companies make it to their shortlist after they apply their filters. The 27 listed companies traded at sufficiently low multiples to finally make it to their universe.

Apart from Nalanda’s universe of 800, there are an additional ~4,500 smaller listed Indian companies. So, individual investors have a far larger hunting ground than Pulak Prasad. However, I suspect that an overwhelming majority of these companies would not pass Nalanda’s muster. Something to keep us occupied while waiting for the next market correction!

Thanks for reading! If you found this article insightful, I’d love to hear your thoughts.

My full notes and summary of the book can be found here, if you’re interested!

Onwards and upwards

Hope you’ve enjoyed reading! As always, let me know your feedback and any other companies / topics that are worth a deep-dive.

Sharing some useful websites / tools I use on a regular basis:

Tijori Finance - Indian company financials, benchmarking & knowledge base

Valuepickr forums - Indian investing and company forum

Dataroma - US “super-investor” portfolios

ValueInvestorsClub - international stock deep-dives

International company financials:

Simplywall.st for a quick overview and financials

roic.ai for detailed financials

Yahoo Finance is good for a look at the balance sheet

Morningstar tracks historical efficiency metrics like ROE and ROIC

Portseido - Portfolio performance & asset allocation tracker

A custom multi-reddit for all the reddit investing communities I follow

I was also able to screen 98 companies that met Nalanda’s quantitative requirements using Tijori’s “filter” feature: Link

Returns are quoted in rupees; Source: What I Learned About Investing from Darwin

The return on capital for all Indian firms is published annually by Aswath Damoraran . Refer to “Return Measures > EVA and Equity EVA by Industry > 2. Just India”; 8% including financial firms and 12% excluding them.

I haven’t looked into the earnings for each company in details - so these PEs and ROCEs could include one-offs and non-operating items.

Even the PE of 24.7 is above the historical median NIFTY PE on 20

Downloadable version of Nalanda’s current portfolio holdings: Link

very insightful

This is very useful. Thanks. I would like to speak with you. I am Anand from The Ken. My email is anand@the-ken.com