CreditAccess Grameen [NSE:CREDITACC] - low-cost, customer-centric microlending at scale

The Indian microfinance powerhouse with macro growth opportunities

Summary

CreditAccess Grameen seems to be a compelling long-term investment, as:

The micro-finance industry (MFI) is crucial to financial inclusion in India and is recognized as a “priority sector” for lending by the RBI

The MFI sector has grown by 17% CAGR over FY20-24, or more than twice the overall GDP growth. I expect it to continue growing, as more than 70% of the Indian population is either un-served or under-served in terms of credit

CreditAccess Grameen (CAG) seems to be the best-run and most customer friendly micro-finance company in India offering the lowest average interest rate. Hence, I expect it to maintain or increase its market share in the MFI industry. It is also trading at a reasonable price for the long-term investor.

Detailed analysis follows, covering:

Industry overview

Business model

Management

Financials

Competitive advantages / moat

Runway / future growth potential

Risks

Valuation

Sources

Industry overview

Most investors deem the Indian Microfinance industry (MFI) as “un-investible” for various reasons, many of which are valid. However, this industry is an essential for financial inclusion in the country, as 80%+ of Indians do not have access to the traditional savings and loan industry. Hence, millions of individual Indians and SMEs depend on microfinance for both personal and business needs. The government recognizes this, and has classified MFI as a priority sector for lending.

Traditional Indian banks often overlook rural borrowers due to their lack of credit history and collateral. Additionally, their limited branch networks, concentrated in urban areas, hinder accessibility for rural communities. As a result, nearly half of Indian borrowers rely on NBFCs and MFIs for credit.

Microfinance is not the magical solution to take people out of poverty; it is merely a tool that the poor can use to raise their prospects for an escape from poverty

Recent turbulence in the Indian microfinance industry

Indian MFIs experienced several headwinds in 2024:

Rising delinquencies caused by high inflation, heatwaves and over-leveraged borrowers: Bad loans (91-180 days overdue) increased from 1.2% in June 2024 to 1.9% in September 2024

The gross loan portfolio (GLP) of MFIs shrunk by 3.86% in Q2 FY25

Several MFIs like Spandana Sphoorty and IndusInd Bank had significant write-offs driven by higher NPAs

The Reserve Bank of India (RBI) took notice of the sector's issues and implemented stricter measures; It also banned 4 NBFCs — Asirvad Micro Finance, Arohan Financial Services, DMI Finance, and Navi Finserv over unreasonably high interest rates & fees, aggressive sales incentives and unsustainable business practices (described in detail in this article)

Microfinance loan interest rates

The primary reason that MFIs charge higher interest rate is due to the higher OPEX, transaction costs and higher cost of funding, as shown below. Banks have access to low cost funding via current and savings accounts (4~5%), while MFIs are dependent on the corporate credit market, where interest rates range between 9~11% or higher. However, some un-organized players also take advantage of uninformed borrowers by charging interest rates as high as 5% per month (80% per annum!).

To put this in perspective, the global average interest and fee rate for microloans is estimated at 30~37%, with rates reaching as high as 70% in some markets.

Hence, the ROEs for traditional banks are similiar to MFIs, at around 12~16%, even though MFIs charge twice the interest rate. MFIs also face higher cyclicality, as their borrowers usually have worse credit and are more exposed to socio-political issues and emergencies.

Business model

CreditAccess Grameen’s history

Established in 1999 by Vinatha M. Reddy, inspired by the Grameen Foundation, founded by Alex Counts and Muhammad Yunus, with a grant of US$35,000 (INR ~3 crore)

2009: Paolo Bruchetti, who runs a Dutch-based Asia-focused microfinance fund invested INR 968 crore in CA Grameen; Now own 66.7% of the outstanding shares.

2010: Udaya Kumar Hebbar, a veteran banker, joined as CEO, and has acquired a larger role as MD and CEO since 2016

2018: IPO in August 2018 raising INR 1,131 crore; opened at around 400 INR/share

2023: Ganesh Narayanan was appointed as the CEO , while Udaya Kumar Hebbar continues to oversee the firm as MD

2024: the largest standalone microfinance MFI in the country, with ~5M customers and a loan book of ₹251 Bn. Note: Bandhan Bank is the largest small finance bank, with 35M customers and a loan book of ₹1300 Bn.

Business overview

6% market share in microfinance loans, both in terms of customers and AUM

Customer profile:

99% women borrowers

86% of borrowers are from rural India & 15% urban

97% of loans use the JLG (Joint Liability Group) model, reducing the default risk from individual borrowers

Unsecured, short term loans; Typically used for income generation , education, healthcare, nutrition, housing and emergencies

Focus on keeping interest rates low for customers, with low OPEX, high collection efficiency and low cost of funding

19k employees in total; 96% of these employees are from the local community

Operate 2031 branches across 17 states / union territories; The branch network has grown at 9% CAGR over the past five years; They have been adding around 30~50 districts annually since 2022

Management

Since 2009/2010, when Udaya Kumar Hebbar took over, the bank has professionalized its management and operations

The company has managed to grow the loan book by 15%+ CAGR in the last decade, while still maintaining a healthy balance sheet and provisions. They have also constantly reduced the OPEX & cost-to-income ratio, showing a focus on operational efficiency.

There have been news reports that Paolo Bruchetti’s firm is planning to sell their stake. However, the promoter is not involved in day-to-day operations even today, so I don’t expect any major changes to management team or company culture.

Financials

Unit economics

A survey conducted by the company (page 17) indicated that 64% customers increased their monthly income by 25%~100%; Typical sources of income: agriculture, daily wage labour, livestock and other small businesses

Apart from income generation, the other typical use cases for a micro-loan are education, healthcare, nutrition, housing and emergencies

Average income of rural households is around ₹12,700 per month; using this figure, the average customer increased their income by ₹3175~₹12,700 (25%~100%) per month after interest payments; Annually ₹38,100~₹152,400

The average ticket size seems to be around ₹50,000; Hence the annual returns for a typical borrower are between 76%~300%; Hence, the interest rate charged on a micro-finance loan (19~21%) should be payable, leading to a win-win outcome for both the borrower and the MFI company

However, borrowers also take on significant risk - if their business ventures do not immediately yield positive returns, many would struggle to pay back the loans; In the case of a widespread natural disaster or emergency (like to COVID lockdown), many of these customers struggle to repay their loans, leading to high NPAs (non-performing assets) for the MFI industry

Profitability

Net interest margin has been around 13%, which should lead to a return on equity of 15~20% if NPAs remain similiar to their historical averages

Due to higher NPAs & provisions in the last quarter, ROE has dropped to 10%; However, I expect this to recover in the coming quarters. For reference, their ROE has been 15% on average over the last 8 years.

Capital allocation and dividend

A majority of earnings is funneled into expansion, with around 11% of earnings paid out in dividend

Competitive advantages / moat

CreditAccess Grameen seems to be the highest quality and most customer centric company in the MFI space.

Lowest lending rates in MFI industry

Low OPEX, due to a focus on efficient customer acquisition and branch operations

The widest branch network with local workforce gives them a deep understanding of each district and its surrounding areas

High customer trust & loyalty

84%-88% customer retention rate over the last several years

95% of existing customers are aware that CA Grameen charges the lowest interest rate

Strong internal controls and risk management, evidenced by a spotless legal & governance track record

Conservative balance sheet: the company maintains a high CRAR (Capital to Risk Assets Ratio) of 26%, compared to the 15% minimum recommended by RBI

This has led to a combination of high RoE & low NNPA, compared to their peers.

Runway / future growth potential

Management has guided for an ambitious 20-25% CAGR over the next 4-5 years, with plans to cross ₹500 billion gross AUM by FY28 (currently ₹251 billion in Q2 FY25). This seems ambitious, but achievable, given their track record.

Risks

A primarily unsecured loan book and high income volatility for borrowers could lead to high default rates. They’ve had default rates ranging between 2~4% in the last 10 years, with the exception of COVID, where they increased to 7~8%

High concentration in 3 states (65% of borrowers and 73% of AUM): Karnataka, Maharashtra and Tamil Nadu. Social or political unrest in one of these states could have a significant impact on collection efficiency and delinquencies .

High competition - there are over a 100 MFIs and 9300 medium/small NBFCs; A few examples of high quality competitors: Ujjivan SFB, Equitas SFB, L&T Finance & Can Fin Homes

The evolving regulatory framework could affect their strategy or limit their growth; However, as they are one of the best-run and lowest cost providers in the industry, I don’t think this is a significant risk

Valuation

The valuation summary is shown below.

In a worst-case scenario, returns might be modest, similar to a bank FD (6% IRR)

A more likely outcome (base case) is a 15% IRR

However, if management's optimistic outlook (bull case) materializes, the stock price could double in the coming months, especially if NPAs go back to their average historical levels

This asymmetric risk-reward profile makes it a compelling investment at current prices.

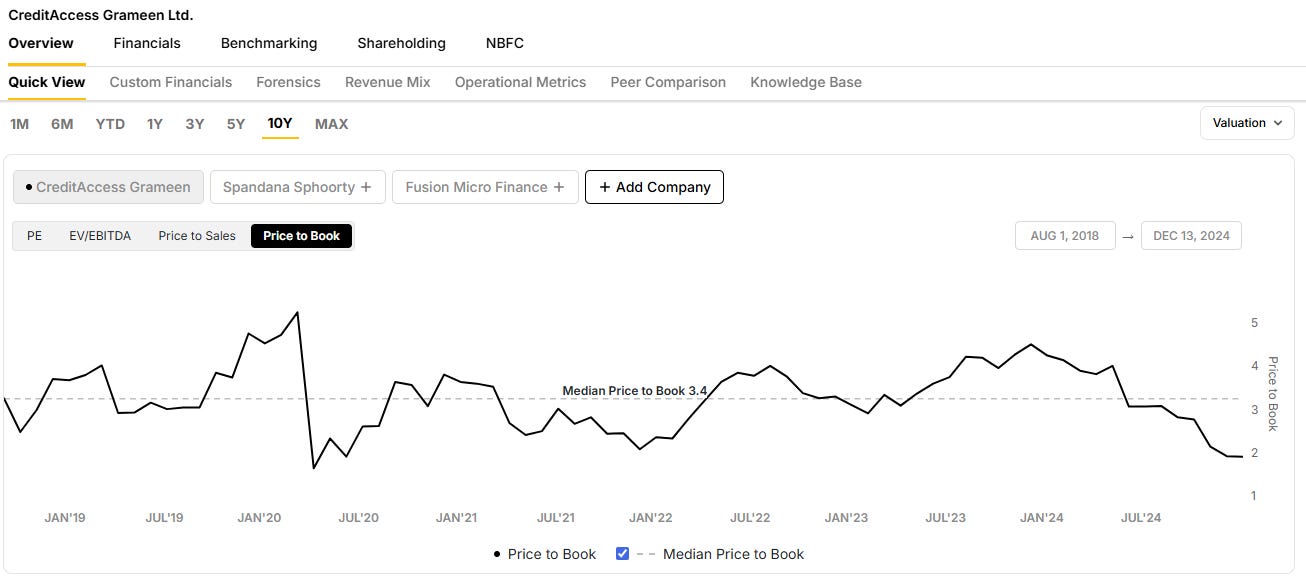

It is also trading well below its historical earnings multiples and price/book:

Conclusion

Prof. Sanjay Bakshi recently mentioned the micro-lending industry in an interview:

"Let’s take the example of what is happening in the micro-lending industry right now. There are a lot of regulatory actions which have resulted in a market-wide selloff in the micro-lending business. But if you look at the history of the micro-lending industry, it has grown and grown over the years. The strong players keep getting better and better and more profitable over time. The weak players or the aggressive players will get dropped out of the game.

But that’s not how the markets are treating the stocks of all the companies in that particular industry. Everything gets sold off the moment you start looking at it from a parimutuel point of view and you start thinking, ‘Well, you know, there is a downturn, but this downturn will actually remove some of the bad practices that are being followed in the micro-lending business.’

Whatever RBI is doing is actually a good thing by stopping all the aggressive lending practices that are being done. Therefore, the more conservative players, the more well-financed players, the more well-run players are going to be better off in the long run. But the stocks are still down. In fact, they have fallen almost as much as the stocks of other ones. So that gives you an opportunity. So that is the lesson that I want to leave the investor: think about the market as a parimutuel system."

Based on my research, CreditAccess Grameen seems to be the strongest player in Indian microfinance (lowest interest rates, efficiently run, healthy capital adequacy and funding). It seems to be following Charlie Munger’s “Win-Win-Win” model.

If you think there any other micro-lenders in India that are better quality than CreditAccess Grameen considering the long-term runway (5~10 years+) - let me know.

Thanks for reading!

Disclaimer: The information contained in this publication is not intended to constitute individual investment advice and is not designed to meet your personal financial situation. The opinions expressed in such publications are those of the publisher and are subject to change without notice. I may from time to time have positions in the securities covered in the articles on this website. I use company declarations and open source information sources believed to be reliable, but their accuracy cannot be guaranteed. The author, shall in no event be held liable to any party for any direct, indirect, punitive, special, incidental, or consequential damages arising directly or indirectly from the use of any of this material.

Sources

https://www.tijorifinance.com/company/creditaccess-grameen-limited/

https://www.bloomberg.com/graphics/2022-microfinance-banks-profit-off-developing-world/

https://mfinindia.org/assets/upload_image/publications/AnnualReports/MFIN%20AR%202023-2024.pdf

For more info on the Indian banking and NBFC industry, I would recommend this video from SOIC & Digant Haria

Appendix

Just went through the Q3 FY25 results. The increase in GNPA (3.99% currently vs. 2.44% in last quarter) and increased ECL provisions (5.07% vs. 3.52%) seems to be due to tighter underwriting norms mandated by MFIN & RBI. I think this should lead to lower defaults in the long term, benefitting CreditAccess, as they avoid lending to high-risk borrowers. The next few quarters might have volatility , because GNPA will probably increase, but the management expects asset quality to normalize after Q1~Q2 FY26. Still seems to be a good long-term prospect at current prices.

The management’s full comments can be found here: https://www.creditaccessgrameen.in/wp-content/uploads/2025/01/CreditAccess-Grameen_Q3-FY25_Result.pdf

Earnings can be found here: https://www.creditaccessgrameen.in/wp-content/uploads/2025/01/CreditAccess-Grameen_Statement-of-Unaudited-Standalone-and-Consolidated-Results_Quarter-Ended_31-December_2024.pdf

Nice writeup. I believe all state government's will end up with Ladli Behena and other populist schemes targeting rural voters which will help MFI players.