Indus Towers - A bet on the future of India's wireless data infrastructure

India's largest mobile tower operator has faced recent headwinds, causing the stock price to tumble. However, I think its long term prospects are still in-tact.

Summary

Indus Towers (NSE:INDUSTOWER) is the largest Indian cell tower company with a history of high ROCE with long term contracts and good visibility of cash flows. Indus had faced headwinds in the last ~2 years, with one of its 4 key Telco customers (Vodafone Idea) coming close to bankruptcy, which has led to deferred payments, write-offs and a large provision in Indus’ balance sheet.

However, looking at the fundamentals and competitive landscape, the stock seems to be trading below intrinsic value in the base case, while only slightly overvalued using pessimistic assumption:

Detailed analysis follows, covering:

The Indian mobile and cell tower industry

Indus Towers is the biggest cell phone tower operator in India with ~30% market share currently. There are 1.4Bn people in India, of which around 80% are mobile phone users, who rely on these towers for mobile connectivity. The wireless data usage per subscriber is currently ~17GB per person per month, growing 14% YoY. American Tower states 2023 expected usage would be ~30GB/month per smartphone user - amongst the highest in the world. One reason for this is that the majority of rural households in India lack wired broadband connections, and use their mobile phones / dongles for internet access.

The wireless mobile market was historically dominated by Airtel & Vodafone, until Reliance Jio’s explosive entry in 2015, which led to a multi-year price war and consolidation across the industry. Jio is now the largest wireless operator, closely followed by Airtel, which seems to have gained a steady hold on the #2 spot . The third largest player, Vodafone Idea, has struggled to stay profitable since Jio’s entry and is on the brink of bankruptcy - a point we will revisit later on in the article.

Earlier, each of the major Telcos put up their own cell towers. However, they realized later that is more economical to run towers in a “shared” model, where multiple Telcos can use a single tower. All of them have subsequently divested their tower units. Airtel, Vodafone and Idea decided to merge their respective tower units into a single entity, forming “Indus Towers” in 2007 and finalizing the consolidation in 2021.

The total cell towers in India are around ~618k by the end of 2022, with Indus owning 31% of installed tower base:

Jio sold their tower business to Brookfield in 2020, forming “Summit Digitel” towers, the 2nd largest tower operator in the country. Brookfield took on a large amount of debt to fund the acquisition. Hence, the unit is operationally profitable, but posted a large net loss due to their interest expenses last year.

American Tower, which is 3rd on the list, is looking to exit the Indian market, citing weak customer financials, presumably due to the Vodafone Idea crisis.

BSNL, which is 4th on the list above, is government owned and the only large player that is both a Telco and tower operator. They are looking to sell some of their legacy towers to raise funds. I assume that part of the sale proceeds would be used to expand its tower footprint to include 25k remote / difficult to reach villages.

Once the sales / acquisitions are completed, the Indian tower market seems to be an oligopoly between Indus, Brookfield, BSNL and whoever takes over ATC’s Indian tower unit.

Indus’ business model

Indus rents land, builds towers and leases them out on long term contracts to the four main Telcos (wireless mobile operators). Each tower can support more than one Telco, with some locations having all 4 Telcos on a single tower. Overall, Indus has 192k towers and 342k “co-locations”, meaning each tower supports ~1.8 Telco tenants. The weighted average remaining life of their current customer contracts is 6.28 years, providing good visibility on future cash flows, as long as the 4 main Telcos remain solvent!

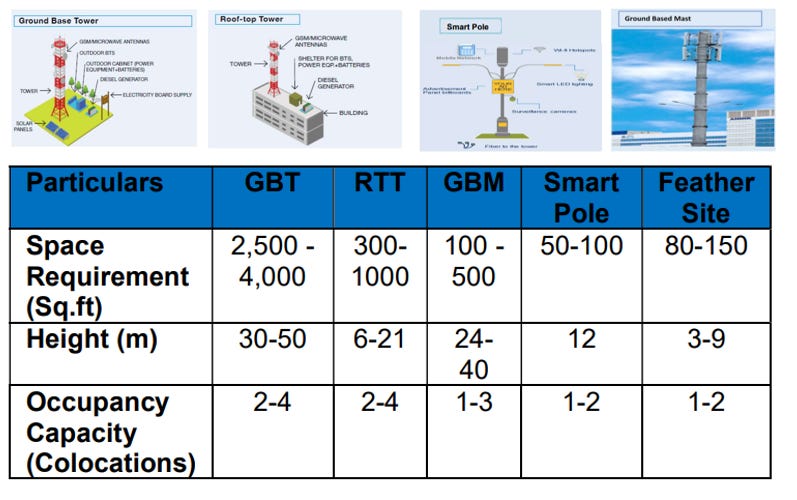

There are two kinds of infrastructure that constitute a telecom tower:

Tower Infrastructure - owned by tower companies (i.e. Indus, Brookfield, ATC) - Steel tower, shelter room, DG set, power regulation equipment, battery bank, security cabin etc. that supports active infrastructure. These are

Active Infrastructure - owned and supplied by telecom operators (i.e. Airtel, Jio, VI), example: Radio antenna, BTS/cell site, cables, Fibre POP’s etc.

Indus Towers has ongoing Master Services Agreements (MSAs) with its customers (Telcos). The MSAs are long-term contracts which set out the terms on which access is provided to the Company’s towers, with all service providers being offered substantially the same terms and receiving equal treatment at towers where they have installed their active infrastructure.

The Vodafone Idea (VI) crisis

Once Reliance’s Jio entered the Indian wireless market in 2015 with an aggressive growth strategy, the incumbent Telcos began to steady lose market share and were forced to reduce APRU (Average Revenue Per User) to remain competitive. Having paid billions to acquire telecom licenses and spectrum, they were also saddled with large debts on their balance sheets. This prompted two of the largest Telcos, Vodafone India and Idea Cellular, to merge, forming Vodafone Idea (VI) in 2018.

The merger was supposed to create synergies, reduce competition and debt over the next few years. However, the combined entity continued to lose market share and weren’t able to raise prices sufficiently. The net debt of VI reached 1Tn INR (1 lakh crore) in 2020, with insufficient operating earnings to cover debt payments. This led to them differing payments to Indus for the last few years and Indus writing off some of these as bad debts. VI continued to struggle since then, with net debt reach 2Tn INR last year. The Indian government finally stepped in, converting some of the debt into an equity stake and becoming the largest shareholder in VI in February 2023.

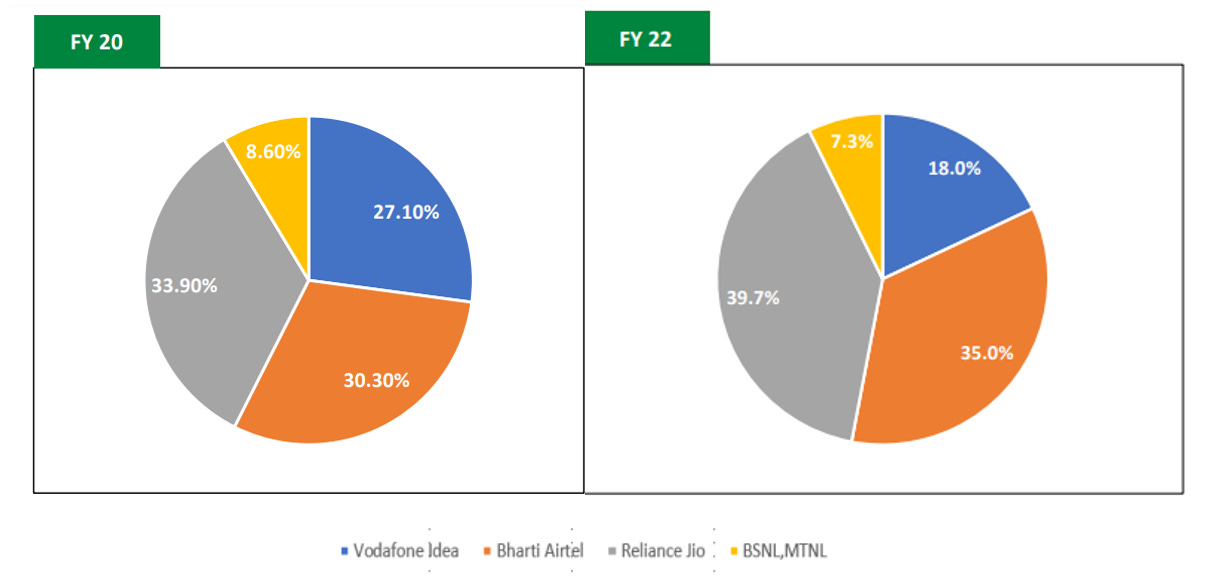

VI still seems to be in hot water: even though it is operationally profitable, it has a humongous debt load, leading it to lose ~70Bn INR per quarter. VI is also not able to keep up with the industry in terms of spectrum upgrades, which is causing some of their subscriber base to jump ship to either Jio or Airtel. Indus’ revenue share from VI dropped from 27% in FY2020 to 18% in FY2022, and is expected to drop further in the coming quarters.

The delayed payments and write-offs have weighed heavily on Indus’ financials, causing their net profit margin to drop from ~20% to ~7% in the quarter ending Jun 2022 and negative 11% in the quarter ending Dec 2022.

I see 3 potential scenarios for VI going forward:

Continued bleeding of subscribers to Airtel / Jio, inability to shore up the balance sheet and eventually shutting down operations

Government increasing their stake and/or merging VI with BSNL

Outright purchase by another private entity or conglomerate, if a new promoter is willing to take on the massive debt load of VI

Even if VI does shut down, their ~226M subscribers would still need mobile services. If a majority of these subscribers move to either Airtel or Jio, the Indian wireless market will turn into a duopoly, which would likely bring down the “co-location” factor from Indus’ present level of 1.8, to levels closer to 1.0~1.1 according to this article by the Ken.

VI represents 18% of Indus’ revenue. If we assume that tenancies are proportional to revenue, that would represent ~62k tenancies. If we remove these from the 342k total tenancies, we arrive at 280k tenancies, which would reduce Indus’ tenancy ratio to from 1.8 to ~1.45, which is higher than the number estimated by The Ken above.

Management

Indus appointed a new CEO, Prachur Sah, in Jan 2023 who replaced Bimal Dayal, who had stepped down in 2022 after 12 years at the company. Prachur Sah is relatively new to Telecom, having spent the previous 22 years in the oil & gas Industry. The CFO and COO are also relatively new, joining in 2021 and 2016 respectively. Hence, the current management do not have a long track record at Indus which we can use to evaluate their performance.

Indus’ board is also peculiar, as it has 7 of 12 members who are associated with either Airtel or VI, which has prompted investors to question whether a conflict of interest exists.

This article by the Ken quotes a former Indus executive as saying:

“Indus Towers’ customers were also its board members. If the company would get in a bunch of other things, they felt serving the telco would take a back seat,” said the former senior executive.

Airtel currently owns ~48% of Indus’ outstanding shares, while VI owns ~21%. However, VI might have to liquidate their stake to shore up their balance sheet, while Airtel lists Indus as an “asset that can be monetized to lighten the balance sheet”, indicating that they might sell their stake, in case they need the extra liquidity in the future. Both Telcos would need to invest significant amounts if they want to upgrade their networks from the current 2G~4G to 5G, so this is a realistic possibility.

Hence, the conflict-of-interest risk is very real. However, Indus’ strategic objectives indicate that financial efficiency and growth would be the focus. Past evidence supports this statement, as they’ve had steady growth in their tower footprint, while maintaining a respectable ROCE of 20%+. If the current management manages to continue the trend of steady growth with prudent capital allocation, it should lead to a win-win-win scenario:

Win for Telcos and Indian mobile customers, with better network connectivity across the country facilitated by higher tower density

Win for shareholders with increasing free cash flows, dividends and growing competitive advantage

Win for employees with business stability and growth opportunities

However, if the 2 Telcos on the board influence the company to make poor choices (e.g. adding towers where multi-customer tenancy is less likely), then it could lead to employees and shareholders paying the price.

Financials

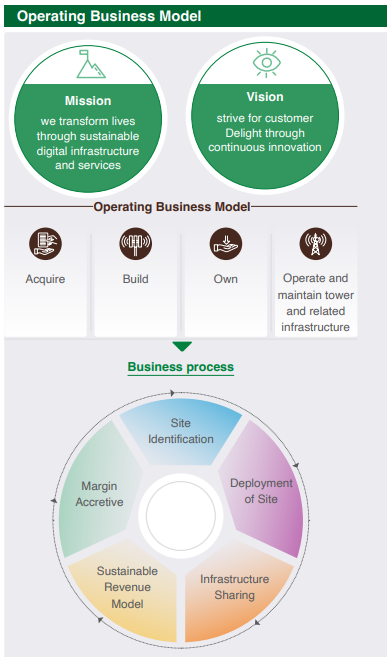

Indus operates as a “passive infrastructure” company (similar to a REIT); A very simplified version of their business model:

Leasing out land

Building and maintaining towers on the leased land

Leasing out these towers to Telcos on long-term contracts

Using cash flows to increase their tower footprint

Asset value

Indus owns 192k towers and lists total non-current assets at ₹378B, which equates to approximately ₹1.97M (or ₹19.7 Lakh) per tower (including antennas, wiring, fibre optical cables etc.)

Indus’ market cap, as of July 2023 was ₹444B, with a net debt of ₹44B (not including the ₹144B in lease liabilities). So the effective EV (Enterprise Value) is ₹488B. Dividing this EV by number of towers, equals to a value of ₹2.54M, or ~1.3 times book value per tower.

The cost of setting up a new tower today is around ₹3~4M. ATC, who are looking to sell their Indian tower business is reportedly looking for US$50k (or ₹4.1M) per tower. Hence, from an asset valuation perspective, Indus would be worth ₹576~₹768B (indicating that Indus is under-valued by 16%~37%). However, the towers are not exactly comparable across different TowerCos (as they include a mix or large and small towers) and these assets cannot all be sold at once, as each sale transaction could take several months. Hence, relying on pure asset valuation is not sufficient.

Assuming a new tower costs ₹4M and the TowerCos want a 10%~15% return on invested capital, each tower would need to generate ₹0.4~0.6M in earnings annually. Indus currently generates an operating profit of ~₹0.44M per tower, which is towards the lower end of this range.

Unit economics

The financials and balance sheet for the last few quarters has been severely affected due to VI’s payment delays. However, there have been some positive developments, after the Indian government’s intervention, with VI clearing a large portion of the outstanding debt in Q1/Q2 2023. Assuming VI doesn’t default on payments in the following quarters, we can look at the unit economics of their tower business.

The revenue from each tower, considering a tenancy factor of 1.78, is ~₹0.9M annually. Electricity expenses for running the towers are charged back to Telcos at cost, so the main operating expenses are repairs, maintenance and employee costs. The operating margin is approx. 50%, equating to a profit of ~₹0.45M per tower. Each of these towers cost Indus ~₹2M to set up, equating to an ROCE (return on capital employed) of ~22% which is approximately what they’ve achieved since FY2020, as seen below.

However, their ROCE would vary significantly based on the sharing factor, as calculated below. I’ve assumed 80% of the operating expenses are fixed based on number of towers and 20% vary based on number of tenancies.

If an operator fixes a base transceiver station (BTS) on a tower, it is considered a single tenancy. For every additional BTS the same operator adds to the tower, it pays only around 10-30% of the full tenancy cost.

Capital allocation and dividend

The company generates significant amount of free cash flow, after operating expenses. Apart from working capital changes, most of the cash flow has been used for CAPEX, dividends and debt repayment.

~44% used for CAPEX

~34% used for growth CAPEX (i.e. new towers and upgrades)

~10% used for maintenance CAPEX

~39% paid out as dividend

~18% paid in interest, repayment of loans / lease obligations (net)

Competitive advantages / moat

Pan-India presence and high barriers to entry; Experience running a large scale, pan-India tower network, well-developed processes, systems and IT infrastructure.

Long term contracts with Telcos & visibility on future revenues; Estimated remaining life of service contracts as on March 31, 2023 is 6.28 Years

Indus has good relationships with all 4 Telcos; Vodafone and Airtel have the added incentive of dividend payments from Indus; There are high switching costs for Telcos to move to a new TowerCo. Telcos don’t have the economic incentive to set up their own towers, as those would have a very low sharing factor and offer low a return on investment

Inflation and cost of new towers: as raw material prices and labor rates increase, costs of setting up new towers would be higher in the future. Hence, competitors would have to spend twice the amount of money as Indus did to set-up a similiar footprint of towers today

Indus is aligned with Indian government’s strategic goal of improving mobile connectivity; It is also the only large TowerCo, which is majority Indian owned

New competitors would face very low return on invested capital if they attempted to set up new towers close to existing Indus towers, as this would lead to a lower tenancy ratio for all players.

Runway / future growth potential

Over the last few years, there has been slow growth in terms of new towers added (~2.8% CAGR), while co-locations shrank between 2017 to 2019 due to the consolidation of Telcos, but has since been growing at ~3.3% annually. The Indus management seem to be expanding cautiously, in line with the broader tower industry in India. This seems prudent, as VI’s future is still unclear at the moment. Hence, the mid-long term tenancy ratio is currently unknow, which is causing the TowerCos to proceed cautiously in terms of expansion.

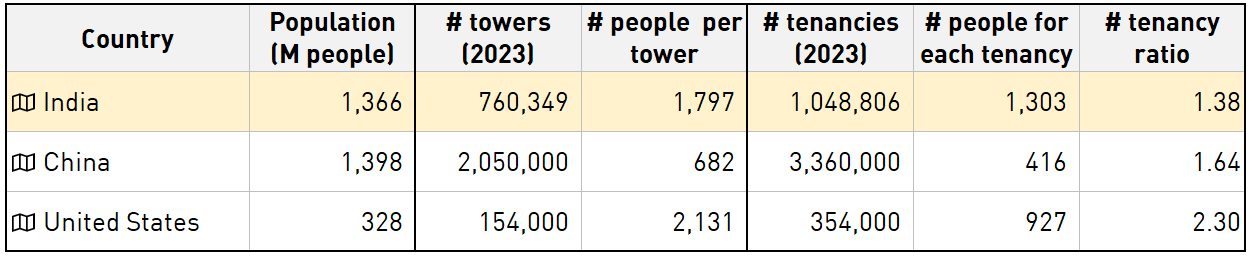

However, looking at other markets like the US and China, there is significant scope to grow the number of towers and tenancies. With a 6%~10% annual growth rate, the total tower footprint would reach 1.1M~1.5M by 2030, which is still lower than China’s 2M towers in 2023. The US has a different model, with larger towers and higher tenancy ratios within the towers, as they have 5 mobile wireless provides with greater than 10% market share, compared to only 3 large Telcos in China and India.

There are also adjacent opportunities that Indus can use to supplement its current income, especially due to their pan-India network of towers and fibre connections. I’ve not considered these, for now, as the Indus management hasn’t indicated any concrete plans for expansion within this space.

Note: many of the newer sites are “smart poles” or “feather sites”, which require a smaller installation area and support fewer tenants per tower.

Risks

VI continues to face financial pressures, delaying or defaulting on payments to Indus - this could significantly impair future earnings

VI’s subscribers largely move to Jio & Airtel, causing the tenancy ratio to reduce to 1.3~1.5

The top 3 customers (Jio, Airtel & VI) represent >90% of revenues and have a significant amount of leverage over Indus Towers. If the profitability in the Indian mobile industry drops, Indus could face margin compression.

Indus’ tower portfolio is older than Summit Digitel’s portfolio. Hence, fewer Indus towers support 4G/5G and would need upgrades, as the mobile industry moves away from 2G/3G to higher speeds.

In-efficient capital allocation on new towers or projects which generate sub-standard returns

Potential disruption from other wireless technologies, such as starlink (although this is probably more relevant for extremely rural geographies which are under-served by the Telcos at the moment)

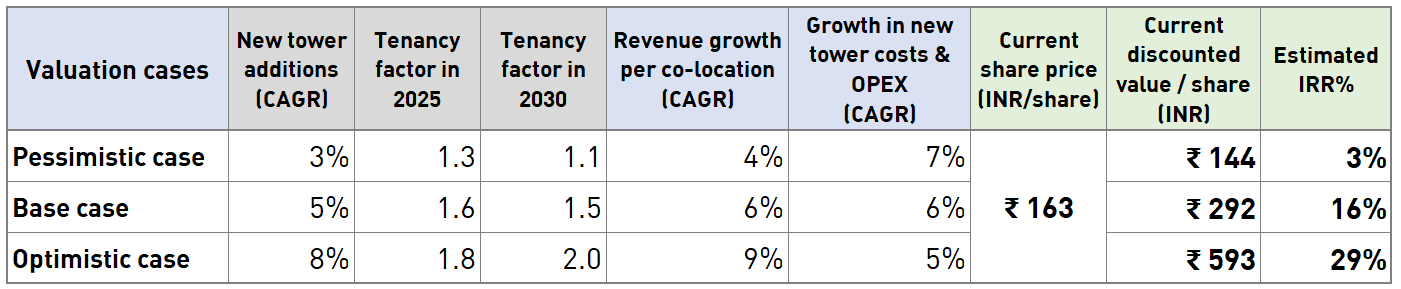

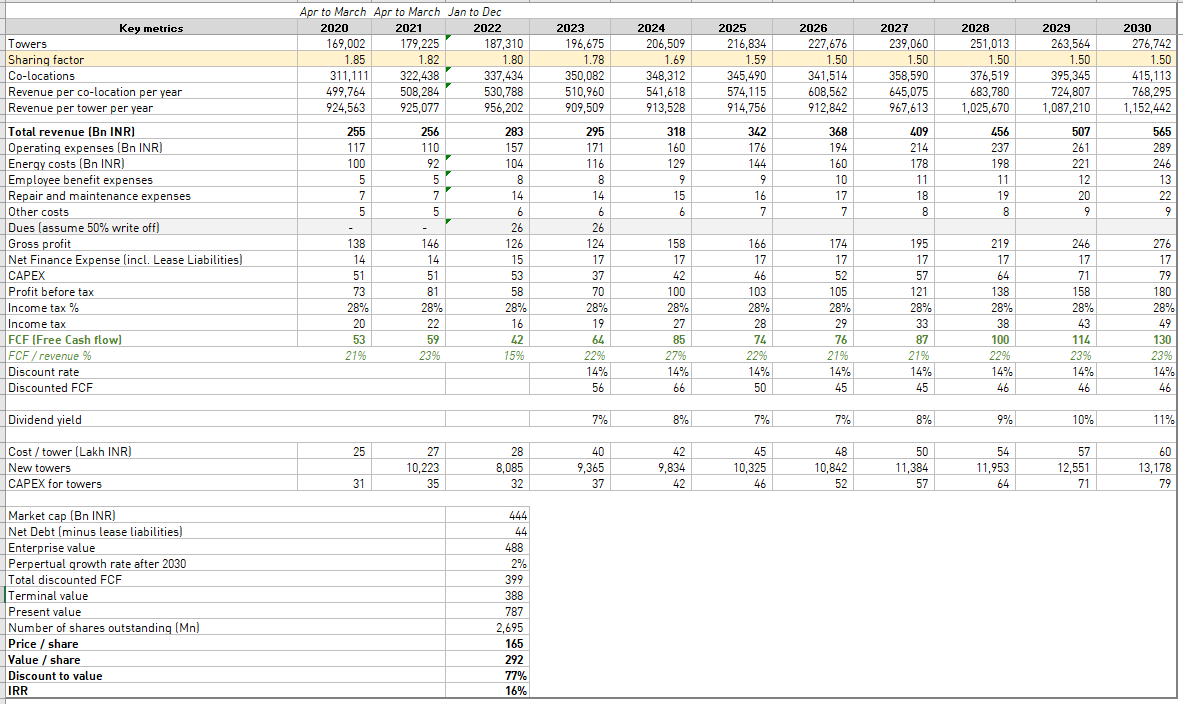

Valuation

Indus trades at INR 444bn market cap and 488bn enterprise value (net debt is 44bn). They will generate free cash flow of INR 60~70bn next year. I’ve used a DCF (discounted cash flow) model with 3 scenarios, as shown below.

The detailed assumptions are below for the base case valuation.

Conclusion

Indus seems to have found a great niche in a growing market with a long runway ahead. However, the management needs to safely navigate the VI crisis and stay focused on profitable expansion.

Personally, I like the risk/reward offered and have invested in Indus, which accounts for ~12% on my India portfolio . I plan to hold on to my position for the next 10+ years (and hopefully, forever). I still expect high volatility in the next 2~3 years, as the Vodafone Idea crisis plays out to completion, so I might get opportunities to also add to my position, if the stock price falls significantly.

Indus would be releasing their next quarterly results and annual report by end-July 2023; I will share an update once that is available.

In the meantime, please share your views and feedback!

Disclaimer: The information contained in this publication is not intended to constitute individual investment advice and is not designed to meet your personal financial situation. The opinions expressed in such publications are those of the publisher and are subject to change without notice. I may from time to time have positions in the securities covered in the articles on this website. I use company declarations and open source information sources believed to be reliable, but their accuracy cannot be guaranteed. The author, shall in no event be held liable to any party for any direct, indirect, punitive, special, incidental, or consequential damages arising directly or indirectly from the use of any of this material.

Sources

Indus quarterly report (Quarter ended March 31, 2023) : https://www.industowers.com/wp-content/uploads/2023/04/3.-Quarterly-Report.pdf

Indus 2021/22 annual report: https://www.industowers.com/wp-content/uploads/2022/08/Indus-Tower-AR-2021-22-Final.pdf

Indus investor relations portal: https://www.industowers.com/investor/

Airtel investor presentations: https://www.airtel.in/about-bharti/equity/results/events-and-presentations

American Tower investor relations: https://atctower.in/en/investor-relations/

Tijori Finance: https://www.tijorifinance.com/company/bharti-infratel-limited/

Telecom Regulatory Authority of India (TRAI): https://www.trai.gov.in/release-publication/reports/telecom-subscriptions-reports

Cellular Operators Association of India (COAI) 2022/23 annual report: https://coai.com/storage/files/2/COAI%20Annual%20Reports/COAI%20AR%20Hi-Res_compressed.pdf

DoT dashboard: https://dot.dashboard.nic.in/DashboardF.aspx

The Ken: https://the-ken.com/story/public-shareholders-may-pay-the-price-for-7b-indus-towers-reluctance-to-diversify/

Summit Digitel annual reports: https://www.summitdigitel.com/page/annual-report

Appendix

Some interesting info I found while doing this write-up.

Subd

Thanks for the context on Indus and the tower market in India. I'm currently an investor in Crown Castle International and it's neat to learn about other tower companies. I love this particular asset class.