Voltamp Transformers [NSE: VOLTAMP] - the "anti-cyclical" power player

The recent promoter stake sale and share sell-off might provide an opportunity to buy a great company at a fair price

Summary

Voltamp is India’s leading manufacturer of transformers for industrial and building applications and has been part of Nalanda’s “permanent portfolio” of India’s best-run companies since 2010.

India’s electrification push has driven rapid growth in the transformer industry but has also brought intense competition and cyclicality. Voltamp’s focus on high product quality, customer trust, and prudent capacity expansion has allowed it to navigate these cycles remarkably well over the past few decades, consistently emerging stronger after every downturn.

The company’s shares had commanded premium valuations in recent years1. However, they have corrected sharply since mid-2024, and again in September 2025 following the promoter stake sale - despite the long-term fundamentals remaining intact. Based on the assumptions below, Voltamp today looks like a great business available at a fair price.

Detailed analysis follows, covering:

Industry overview

Business model

Management

Financials

Competitive advantages / moat

Runway / future growth potential

Risks

Valuation

Sources

Industry overview

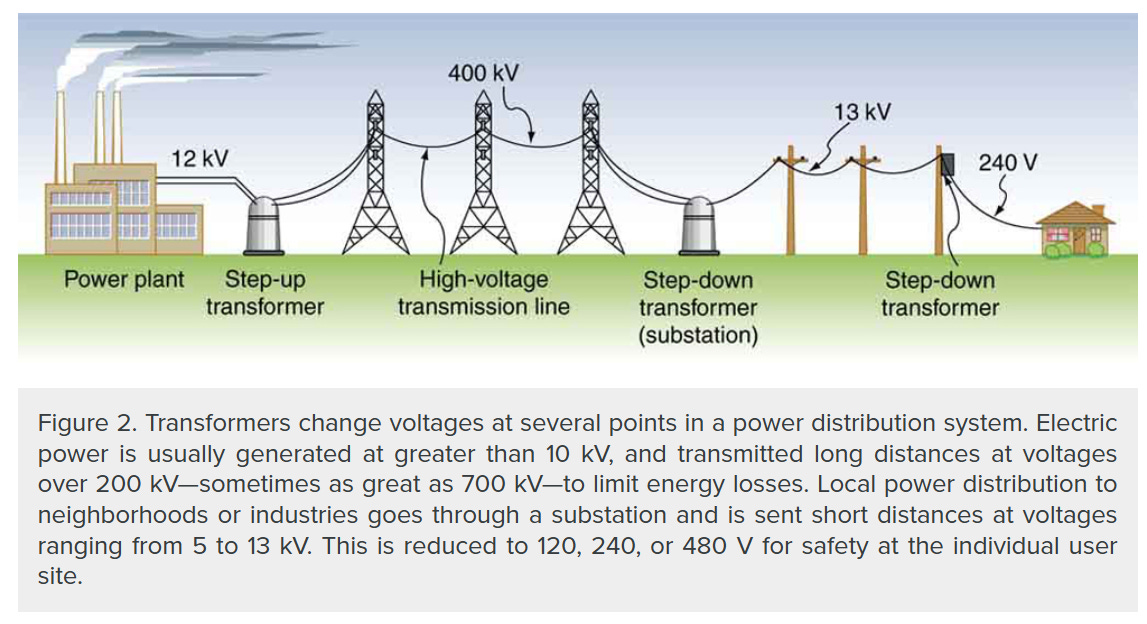

Voltamp primary manufactures “step-down” transformers, that convert high-voltage power to usable electricity for industrial facilities (factories, Tech parts, data centres etc.). They also sell “step-up” transformers for power transmission, but to a much smaller scale compared to the “step-down” category.

Voltamp primarily manufactures “step-down” transformers, which convert high-voltage power into usable electricity for industrial facilities (factories, tech parks, data centers etc.). The company also produces “step-up” transformers for power transmission, though this segment remains much smaller in comparison.

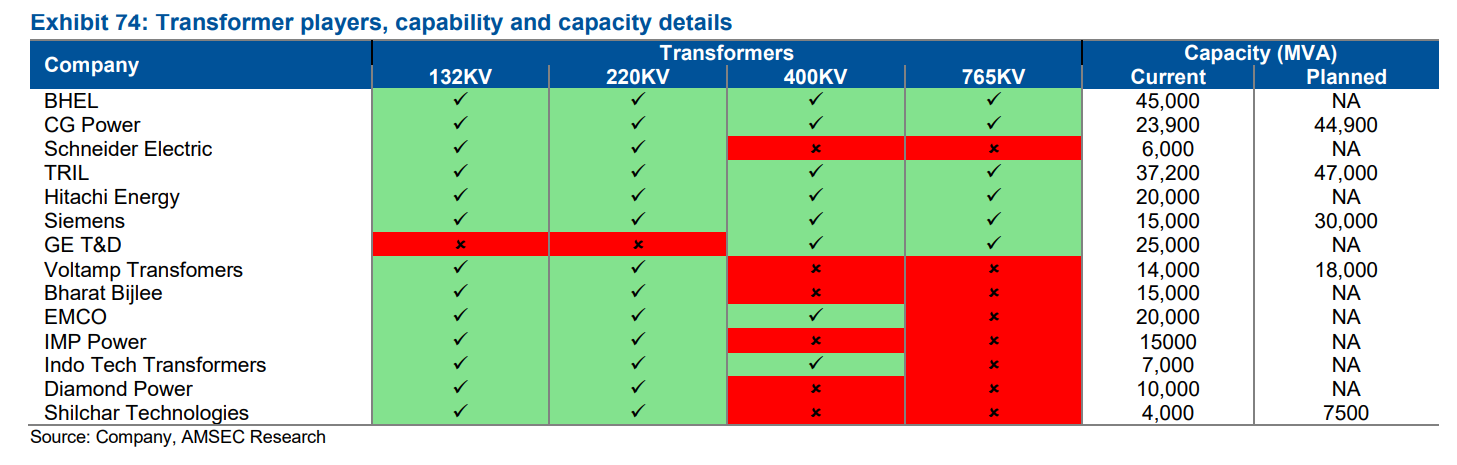

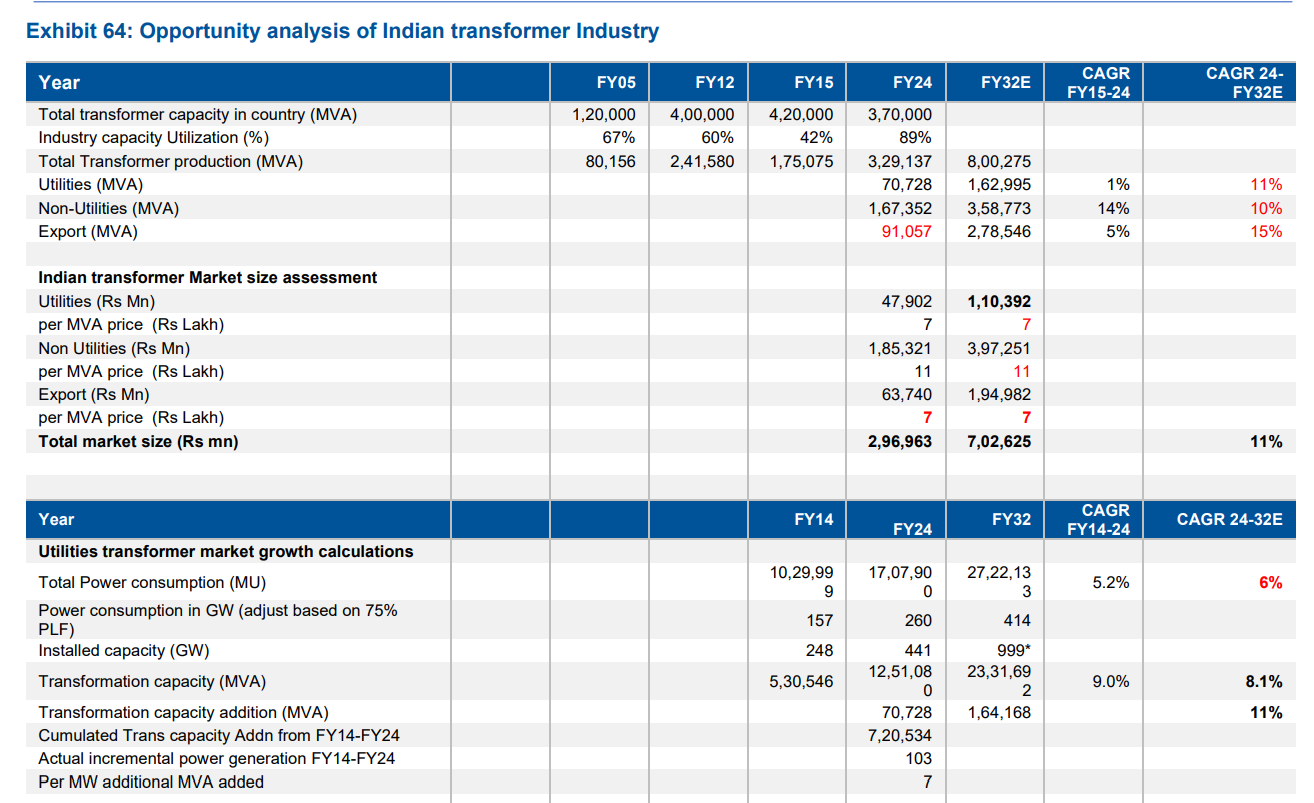

The Indian transformer industry is large and fragmented. Over 300 manufacturers supply India’s power & distribution transformers, but only ~20 are major organized players. Many firms cater to small-scale distribution transformers (<33kV), though some are scaling up into the organized segment. Voltamp operates in the small-mid sized segment (11–220 kV range), with a ~15% market share in organized industrial-application transformers and ~35–40% share in dry-type transformers.

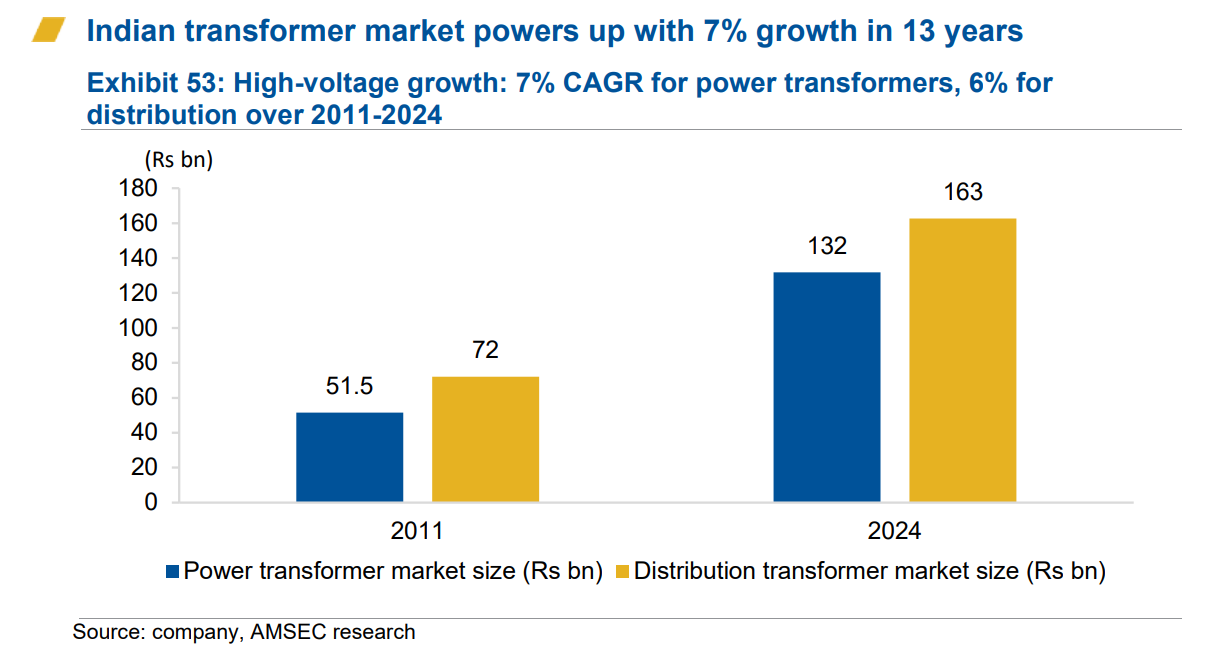

Industry growth has been steady at ~7% CAGR over the last decade, fueled by government electrification schemes and industrial expansion.

Looking ahead over the next 5~10 years, the outlook appears positive: a massive ₹11.2 trillion government capex budget for FY26, renewable energy projects, data centers, metro/rail electrification, and PLI-driven factories all require transformers.

Notably, the unorganized sector still holds ~60% share in distribution transformers, keeping pricing very competitive. However, rising quality needs and scale are shifting more business to reliable, organized suppliers. Hence, I expect Voltamp to grow revenues faster than the overall industry.

Business model

Voltamp’s product range spans:

Oil-filled transformers (up to 160 MVA, 220 kV) for utilities and industries: 77% of sales. These include:

Power transformers (33 KV to 220 KV)

Distribution transformers (Up to 33 KV)

Cast resin dry-type transformers (up to 33 KV) for indoor use like commercial buildings and data centers: 17% of sales

Services & others products: 6% of sales

Service / total lifecycle management over transformer lifespan (30~60 years)

Assembly of Unitized Substation (USS) and ring main units (RMUs)

Voltamp is overwhelmingly domestic-focused. In FY2025, ~98% of revenue came from India, with exports only ~2% (despite sales to 27 countries.)

Over the last decade, Voltamp has had more demand than production capacity, and hence only selected profitable and financially stable customers. Share of public sector revenues dropped from ~100%+ in the 1960s to 10% today, with the private sector contributing to 90% of revenues.

Management

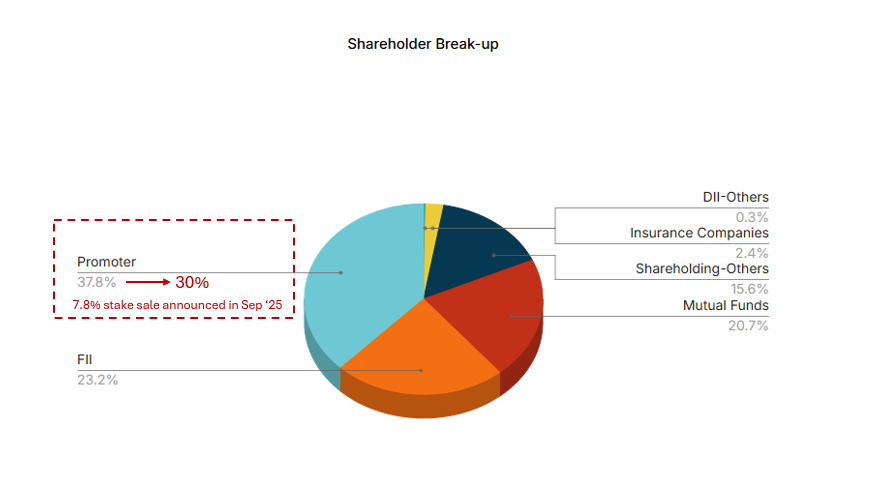

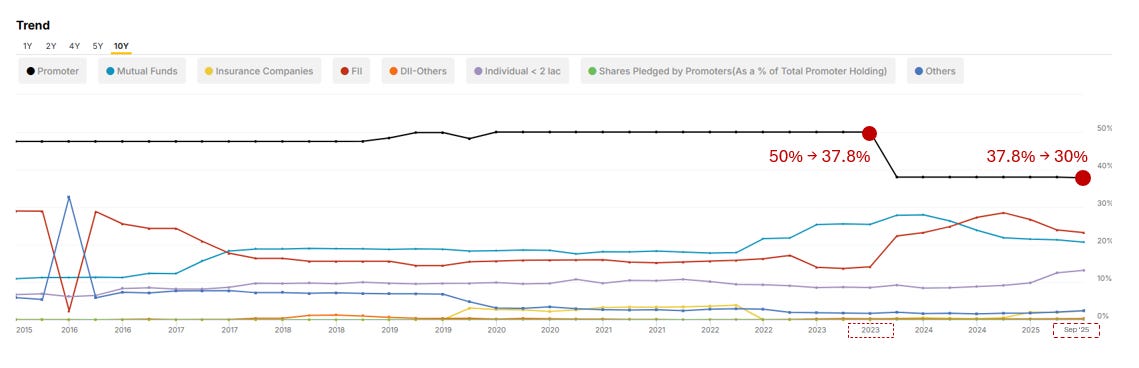

Voltamp is led by the Patel family, who have steered it for decades with a conservative, execution-focused approach. Kanubhai S. Patel (67), Chairman & MD, and his son Kunjal L. Patel (52), Vice-Chairman & MD, together own ~37.8% of the company. However, after the recently announced stake sale, their shareholding would reduce to 30%.

This would be the second time the promoter has reduced their stake, with the earlier sale happening in 2023; I don’t see this a cause for concern, as the promoters would still retain a significant stake post reduction worth ₹22b (US$ 250M).

They’ve maintained exemplary integrity & prudence (e.g. zero debt for 24+ years) and consistently balanced growth with shareholder returns. The Patels are known to “under-promise and over-deliver,” evident in Voltamp’s steady rise without flashy announcements.

Key person risk is mitigated by succession planning: the second generation (Kunjal and family) is firmly involved, and professional management handles daily operations (the CFO and COO are career executives).

Minority shareholders are treated equitably – e.g. timely dividends, no related-party shenanigans. The Patels take a conservative salary: in FY25, combined MD remuneration was ~₹139 Mn, about 4% of PAT, aligning their incentives with performance (they paid themselves ~1% of PBT each, per policy).

No share dilution has occurred in over a decade – shares outstanding ~10.1 million since listing – indicating discipline in capital raising.

Financials

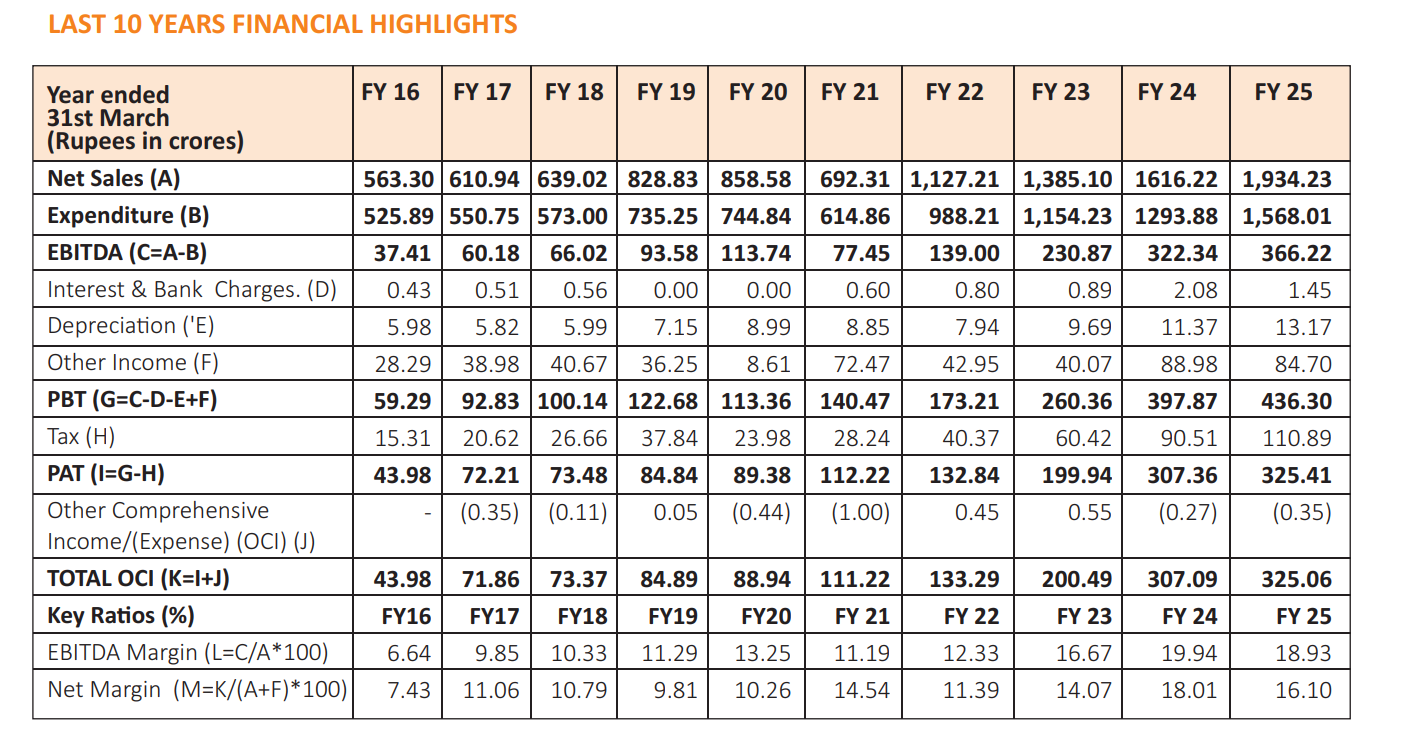

Voltamp’s financial profile is impressive to say the least. Over the past 10 years (FY16 → FY25):

Revenue CAGR was 14.7%

PAT CAGR was ~24.9%

Net margin grew from 7~10% to 16~18%

ROE of 22% and ROCE of 27% in FY25

Net cash and investments of ₹10.8 Bn (14% of market cap); composed of:

Bonds: ₹4.5 Bn

Debt funds: ₹3.7 Bn

Equity funds: ₹1.1 Bn

Cash & liquid investments: ₹1.5 Bn

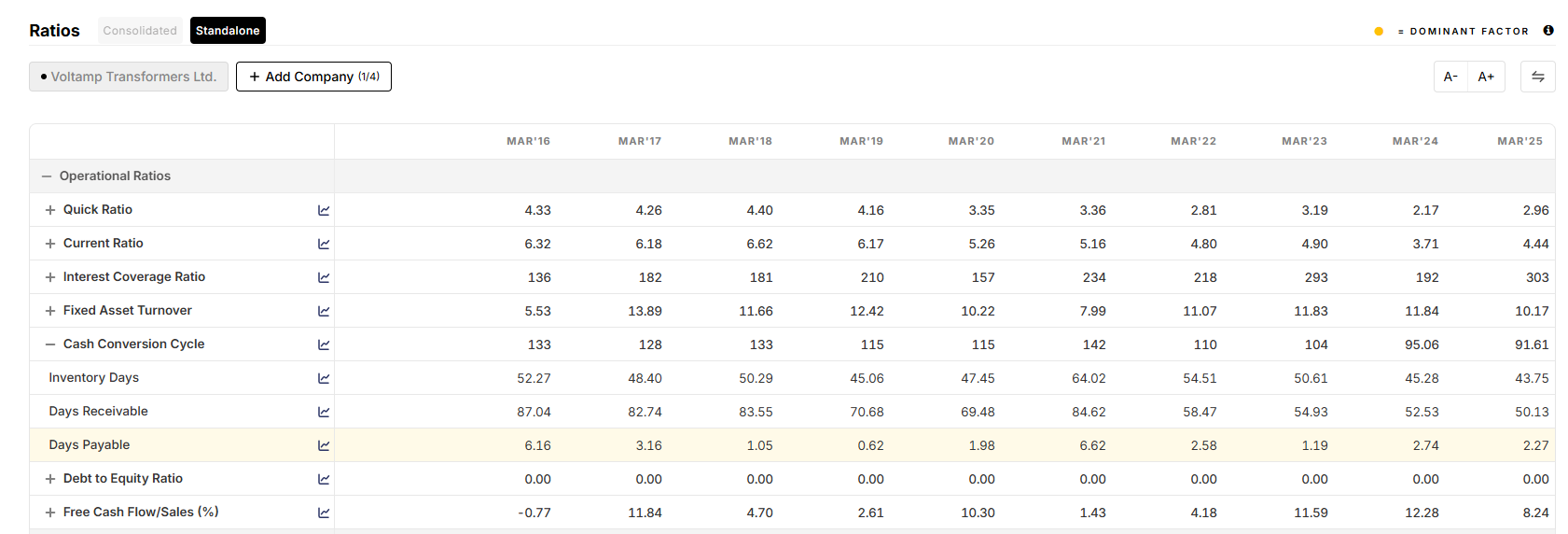

The company converted a high portion of profit to cash – CFO was 94% of EBITDA in FY24 – indicating low working capital drag.

Even though revenues dipped significantly during Covid (FY21), they remained profitable on an operating income basis and their margins remained 10%+ due to their investment income.

Another interesting fact: in past 10 years, Voltamp have paid their suppliers in 2~3 days (compared to their competitors who pay suppliers in 80~100 days!). This probably gives them lower sourcing prices and reduces Forex risk.

Capital allocation and dividend

Use of operating cash flow in the last 10 years of ₹9.5 Bn (source):

Accruals & investments :₹4.4 Bn (46%)

Dividends:₹3.3 Bn (35%)

Capex: ₹1.7 Bn (18%)

A majority of the capex above was spent in the last 3 years a new transformer factory (up to 250 MVA class) that will raise manufacturing capacity from 14,000 to 20,000 MVA per year (+43%). The current expansion is its first major growth capex since 2009, as there was over-supply in the market for most of the last decade.

The company doesn’t believe in acquisitions, preferring to build up capacity on their own, as capacity additions can be done relatively quickly.

Competition & Positioning

Voltamp faces a mix of large diversified rivals and niche local players. Its competitive landscape can be split by voltage class:

High Voltage (132–220 kV) Power Transformers:

Bharat Heavy Electricals (BHEL)

CG Power (Murugappa Group)

Siemens (now merged with Siemens Energy/Hitachi ABB for grid business)

Transformers & Rectifiers India (TRIL)

International competitors like TBEA (China) and Toshiba (Japan)

These players often supply utilities and state networks. Voltamp, despite lacking the might of BHEL or Siemens, holds its own in this segment by focusing on private sector orders and custom specs. Above 220 kV, competition thins out to a few global players – Voltamp historically didn’t serve >220 kV, but with new capacity up to 250 MVA, it may start inching into that territory. However, limited competition above 220 kV also means a higher bar of entry (and lower Voltamp exposure so far).

Medium/Low Voltage (≤132 kV) Distribution & Dry Transformers:

Bharat Bijlee (BBL) – another old transformer maker;

TRIL – focuses on utilities;

Shilchar Technologies – specializes in smaller transformers;

Indo Tech, Kirloskar Electric

Several other smaller / unorganized players (300+)

Despite this crowd, Voltamp has carved a top-tier position: It is often the go-to for private projects where reliability is paramount (refineries, steel plants, IT parks). The company claims 15% share of the organized market for industrial application transformers.

Many competitors have struggled: e.g., EMCO, a once-major player, went insolvent, and others like IMP Power have had persistent losses. In contrast, Voltamp thrived by cherry-picking customers and staying out of cut-throat low-end tenders. Its brand is associated with quality and longevity – a huge differentiator when the product life is ~25+ years. Customers like Reliance, Ultratech, or Indian Oil can’t afford failures, so they stick with proven suppliers.

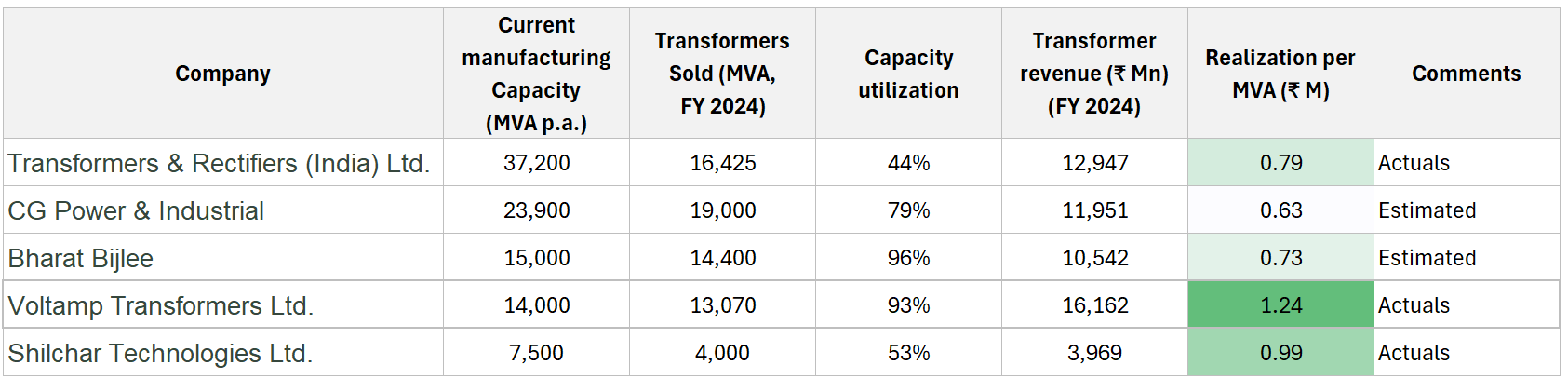

Voltamp has relatively highest realization per MVA (as seen in the table below), demonstrating their selectivity in bidding for tenders. Note: the companies listed below operate in different niches and are their product lines are not directly comparable.

Competitive advantages / moat

Install base: ~950 of India’s top 1,000 companies have Voltamp transformers installed at their facilities. This creates a virtuous cycle: new projects often specify or prefer vendors who’ve delivered reliably before. Voltamp’s brand stands for quality Indian transformers

Trust from marquee customers like L&T, ABB, Siemens, Tata Projects. This helps Voltamp win repeat business. A lesser-known maker simply can’t offer the same peace of mind to a refinery manager or data-center engineer.

Pan-India support network (16 branch offices) ensures quick service response, which many smaller peers lack.

Technical Know-how: Voltamp secured a technology transfer from HTT, Germany back in the 1990s for cast resin dry-type transformers. This gave it a two-decade head-start in mastering dry-type designs that others found hard to crack. The result: Voltamp holds ~40% share in India’s organized dry-type transformer market and has over 22,500 dry transformer installations nationwide.

Fortress-like balance sheet allows them the freedom to be selective during tenders and maintain their high margins

Taken together, these factors don’t form an impregnable moat , especially in the commoditized transformer segments. However, Voltamp should maintain an edge in segments where performance, customization, and service matter.

Runway / future growth potential

The ongoing industrial capex upswing, expected to continue for decades, should provide a strong tailwind. The company has highlighted a robust enquiry pipeline with no signs of a slowdown in its addressable segments.

Demand-supply gap in power infrastructure & utilities: India will continue to be power hungry going forward. The government’s Revamped Distribution Sector Scheme (RDSS) and continued spending by Power Grid and state discoms ensure a baseline growth for transformer demand ~7–10% annually in the utility segment

Data centers and commercial buildings: The digital boom (cloud computing, 5G, etc.) is driving a surge in large data centers and high-end commercial real estate. Some estimates peg data center power infra growth at 20%+ CAGR near term. These facilities typically use dry-type transformers for safety, where Voltamp is dominant

After-sales service scaling: Voltamp’s installed base is aging – many transformers supplied in the 2000s will come up for mid-life overhauls or replacement. The company has started focusing on the services & spares business, which grew to ₹757 Mn in FY24. Management expects service revenue to double to ~₹1.6 Bn by FY27 (30% CAGR).

Export Potential: Currently 2% of sales, exports are not a focus – but they present optionality. Voltamp has exported to Middle East, Africa, and SE Asia on and off. With its new capacity, if domestic demand ever softens, the company could pivot to export markets for growth. The global transformer market is vast, and Indian manufacturers have a cost advantage in medium-range transformers, as demonstrated by Shilchar Tech.

Critically, growth doesn’t require heavy reinvestment beyond the current capacity expansion. The business generates so much cash that future growth can likely be funded internally without issue. This means Voltamp can grow while still paying dividends – a rarity.

Risks & watch-outs

Cyclical downturn in capex: A sharp economic slowdown or postponement of private capex (due to recession, overcapacity in user industries, etc.) would hurt Voltamp’s order inflows

Rising competition is the most tangible risk: several players are expanding capacity (including Voltamp itself). If supply starts exceeding demand, price undercutting could ensue. In an over-supply situation, there is good probability that margins will revert to 10~15% for several years.

Raw material & supply chain volatility: Copper, electrical steel (CRGO), insulating oil – these raw materials form ~75% of Voltamp’s cost. Sudden spikes in commodity prices & rupee devaluation can dent margins if not passed through.

Execution Risk on New Capacity: the new plant for 250 MVA transformers could face cost overruns, delays, or technical issues in ramping up. Also, entering the higher MVA class means competing in a slightly different league (with BHEL/CG etc.). If the new products don’t meet expectations or face quality issues, Voltamp’s reputation could take a hit.

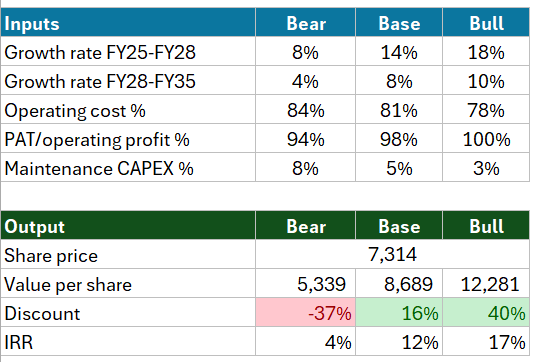

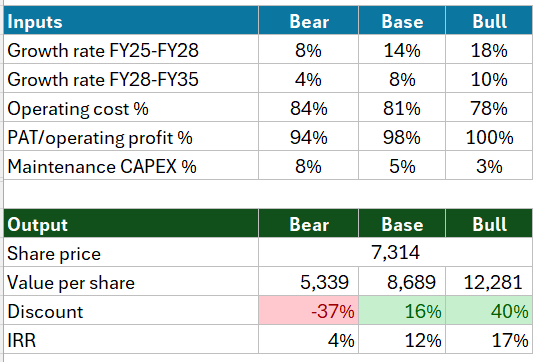

Valuation

The main factors influencing future value are the growth rate, capacity utilization and operating margins

The stock seems reasonably priced at 22x earnings (4.5% earnings yield). The current valuation seems to assume a growth rate of ~10% annually for the next 10 years, which is fairly conservative given the planned expansion which will increase capacity by 43% in the next 2-3 years.

Details can be found in the sheet below.

Conclusion

Voltamp is one of the rare companies that pass all of Nalanda Capital’s filters, while remaining reasonably priced. Hence, it has found its way into my portfolio, where it will probably remain for the next few decades.

Thanks for reading and let me know what you think!

Disclaimer: The information contained in this publication is not intended to constitute individual investment advice and is not designed to meet your personal financial situation. The opinions expressed in such publications are those of the publisher and are subject to change without notice. I may from time to time have positions in the securities covered in the articles on this website. I use company declarations and open source information sources believed to be reliable, but their accuracy cannot be guaranteed. The author, shall in no event be held liable to any party for any direct, indirect, punitive, special, incidental, or consequential damages arising directly or indirectly from the use of any of this material. The author is not SEBI-registered.

Sources

https://www.voltamptransformers.com/investors_desk/annual-reports

https://www.tijorifinance.com/company/voltamp-transformers-limited/

Appendix

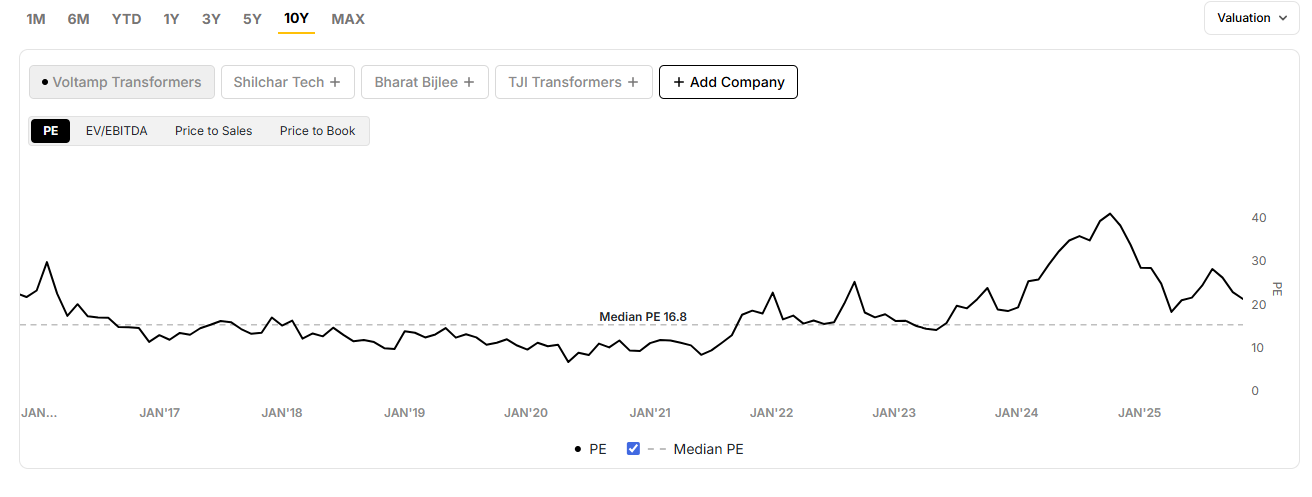

The company traded at 30~40 PE (2~3% earnings yield) during most of 2024, but now trades closer to 22 PE (4.5% earnings yield)

The transformer industry is expected to continue growing inline with India’s GDP for the next few decades:

Thank you for the post. Have the promoters publicly clarified purpose behind their stake sale? Are they using the proceeds for some new business? Is there a risk they totally exit in the future?

For the revenue table comparision, I think the data is incorrect. Could you please check it again.