Looking Back: The Open Source Portfolio in 2025

Reviewing the underlying portfolio quality with a "Fundmith lens"

Transparency is the core value of this newsletter. As we close the book on 2025, I thought it would be a good time to reflect on the year’s highlights and lowlights.

The Substack

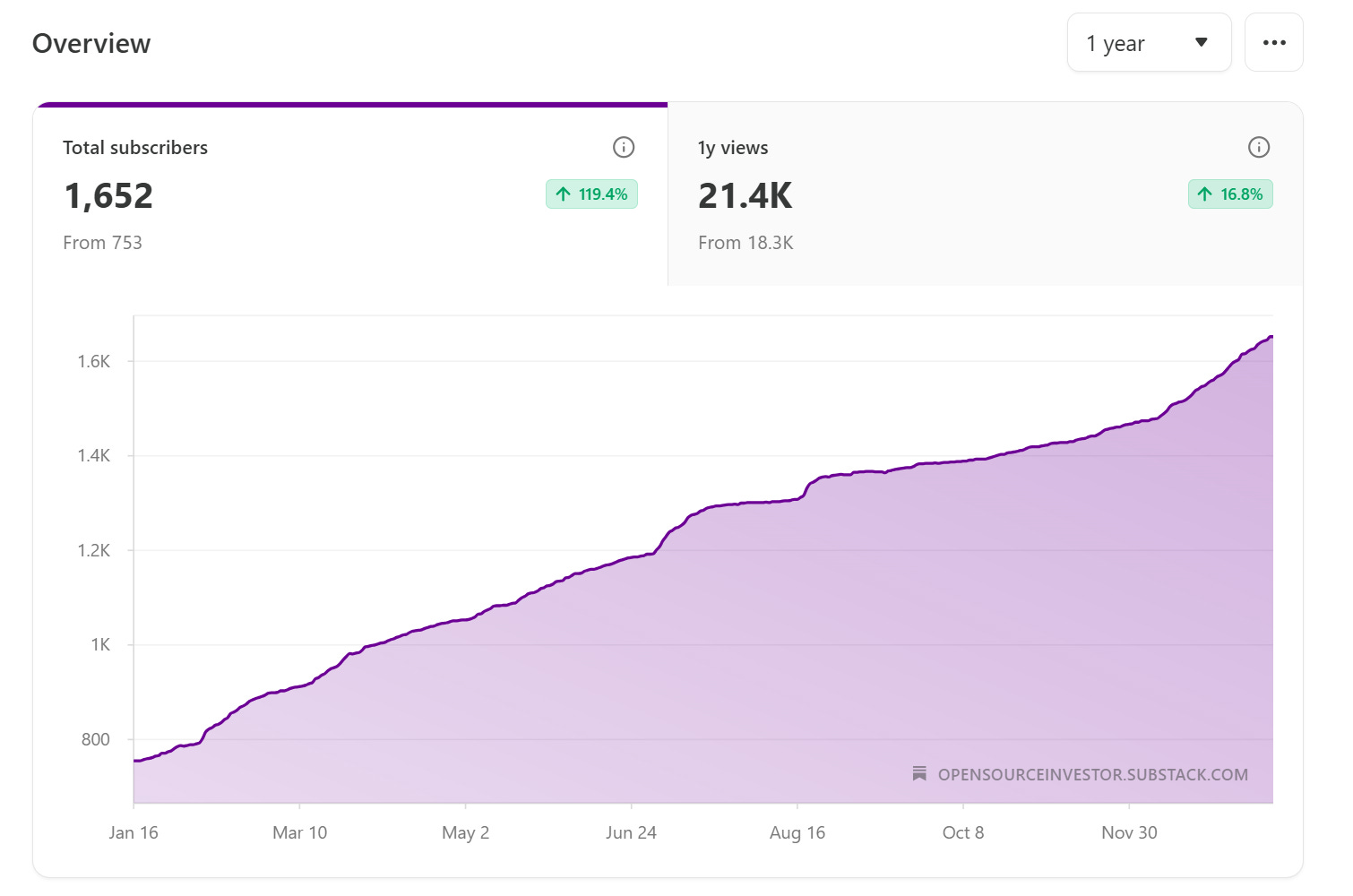

I started this newsletter in December 2022. Since then, I’ve published seven companies deep-dives (listed below) and five other investment-related articles. Hypothetically, if you had invested in this portfolio sequentially since the first date of publishing, the annual return would have been 27% CAGR over the last 2.5 years.

Since the beginning of 2025, my subscribers have grown from ~750 to 1650, growing by 119% CAGR (significantly outperforming the portfolio’s 27% returns!)

Overall portfolio performance

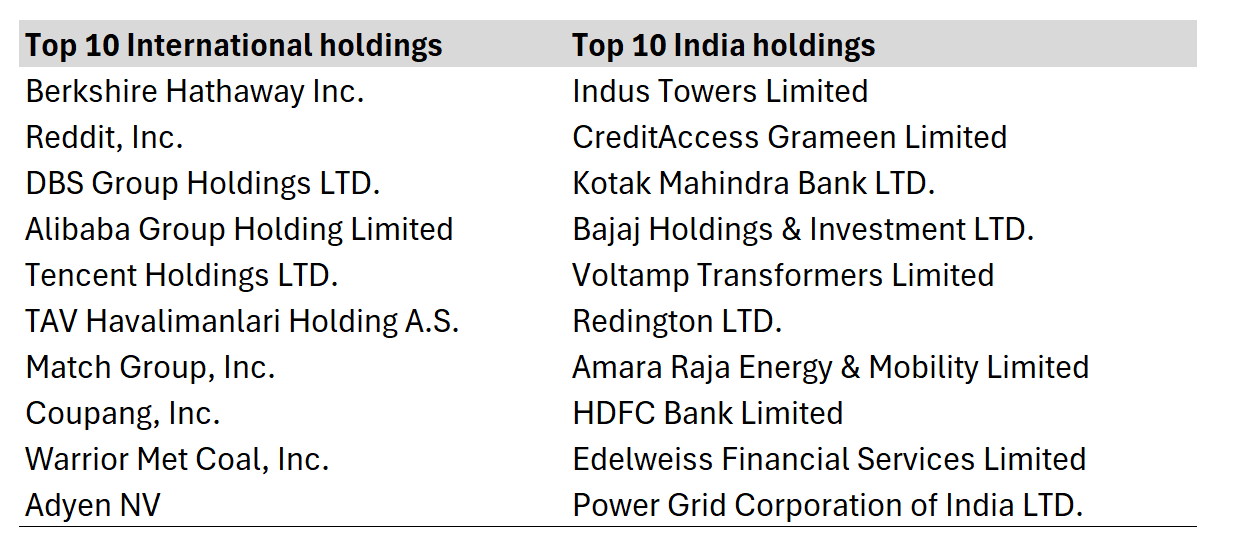

The largest current holdings across my international and India portfolios:

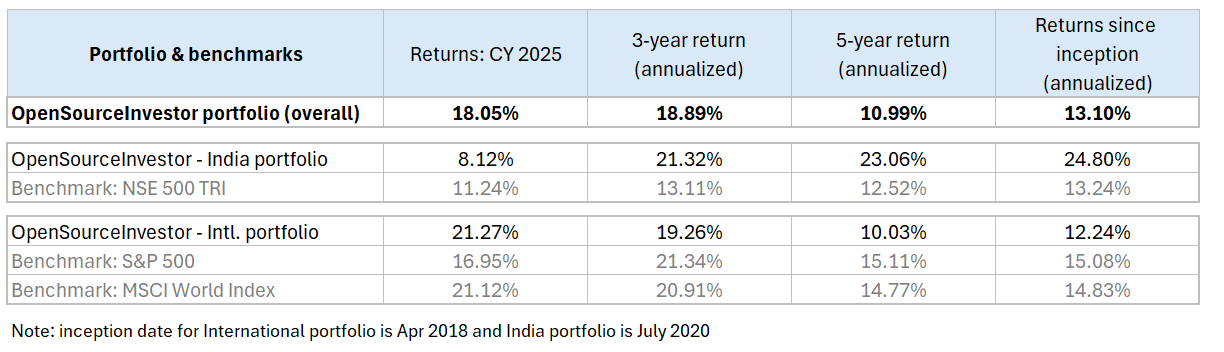

In 2025, the India portfolio had mediocre returns of 8%, while the international portfolio outperformed at 21% return. However, since inception, the India portfolio has significantly outperformed with a 24% CAGR, compared to the international portfolio’s 12% CAGR.

The international benchmarks (S&P 500 & MSCI) have had a great 5-year run with 14~15% returns, primarily driven by the “Mag 7”.

So, should the intelligent investor hang up their hat and go all-in on the index? It is a solid strategy, and one that I would recommend to the 99% of the investing public who would rather spend their time on other pursuits.

I still believe a well-selected portfolio of high quality companies will outperform over the long term, as proven by these 50 super-investors since 1965. One of the most prominent among them is Terry Smith, whom we will meet in the next section.

Terry Smith & Fundsmith

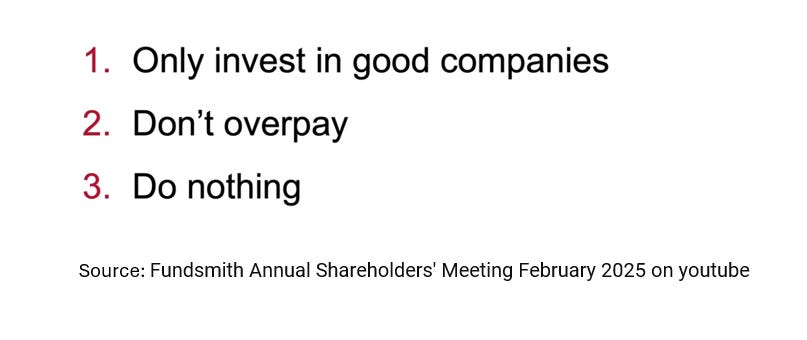

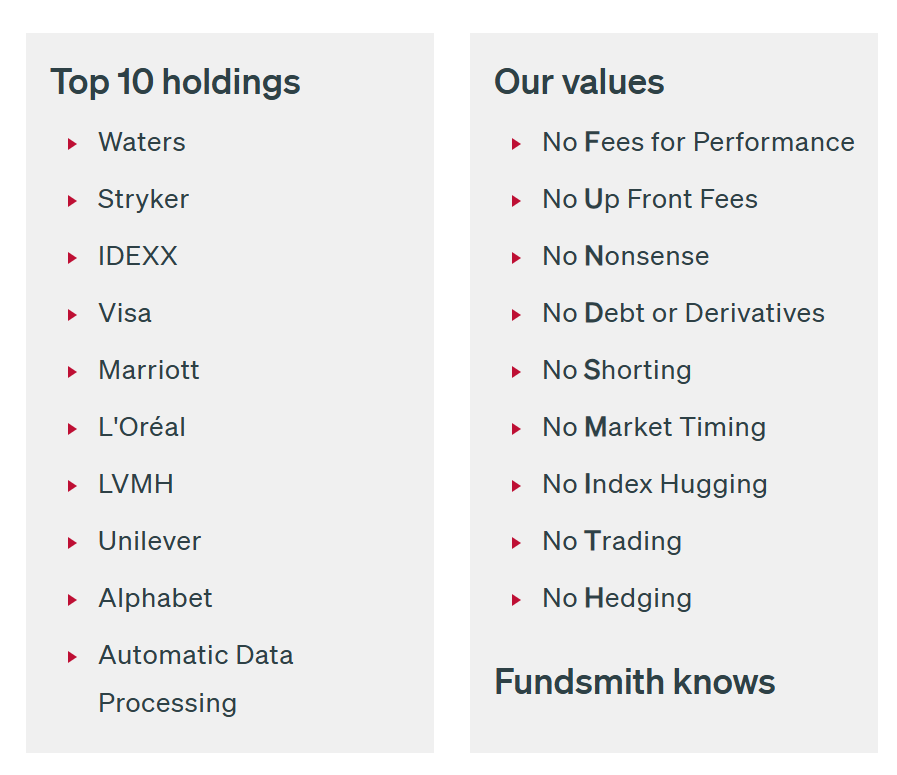

Terry Smith has been one of the UK’s best investors in history. Although, his flagship Fundsmith Equity Fund had a mediocre year in terms of returns, it has managed to beat the index with 13.8% annual returns since 2010. I am a fan of his “no-nonsense” approach to investing, summarized below:

The Fundsmith portfolio as of Dec 2025 demonstrates this strategy:

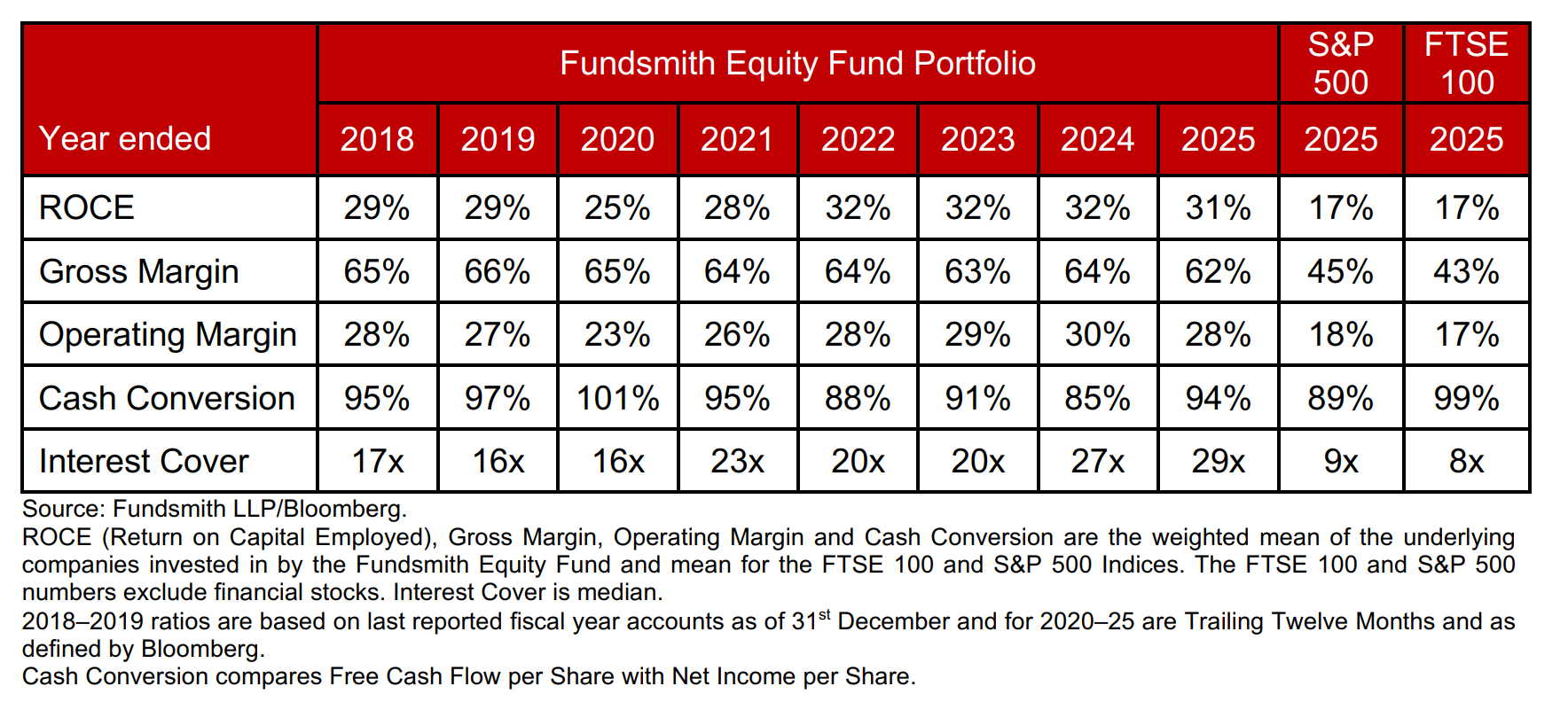

I particularly like the way they assess the quality of their underlying portfolio (shown below). So I’ve decided to borrow the same approach for my own portfolio review this year, a.k.a. “steal it with pride.”

The Open Source Portfolio

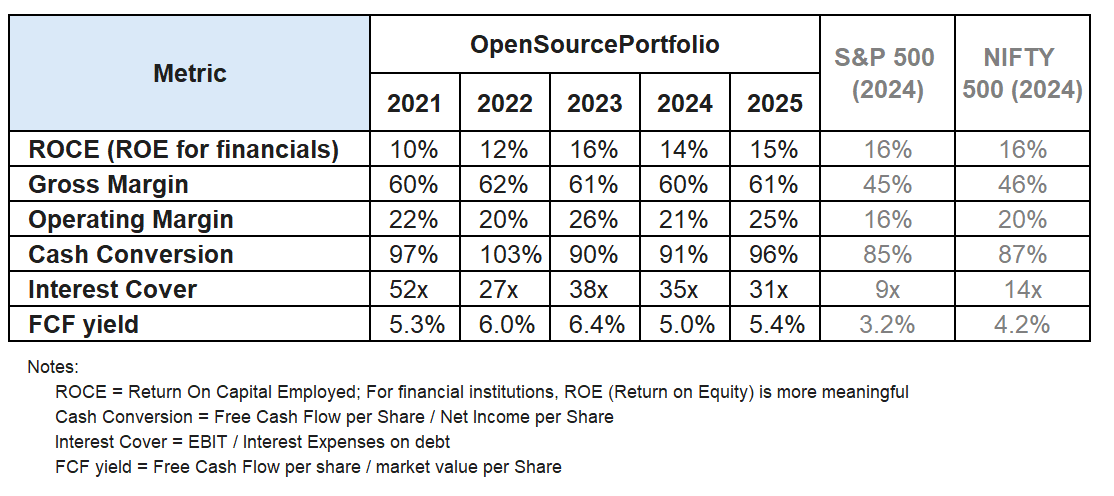

Using Fundsmith’s value lens, I compared my portfolio to the S&P 500 and NSE 500 indices:

Some things that stand out:

Portfolio ROCE is slightly lower than the indices, as I have a mix of mature high-ROCE companies and early-stage / high growth companies (which I believe will generate high ROCE in the future)

Interest coverage of the portfolio companies is 2~3 times higher than the index, due to the preference for low-debt or no-debt companies.

The portfolio FCF yield is 5.4%, higher than the indices at 3-4% due to the preference for cash-generating companies. Interestingly, for the S&P 500, the FCF yield of the mag-7 stocks are at ~3% and the rest of the index is at ~5%.

In terms of weighted average earnings growth in 2025, the portfolio grew by 11%, which was similiar to the S&P500 at 12%.

We can categorize the portfolio using ROCE as a proxy for business quality & FCF yield as a proxy for how highly valued the stock looks (as low FCF yield indicates a high PE ratio).

The obvious preference would be to buy more companies in the top-right bucket, which earn high rates of return and can be bought “cheap” (i.e. at a high cash flow yield). However, I believe the companies on the bottom-right are equally interesting either because:

They will continue to generate a high FCF yield with predictable earnings streams

or

Grow owner’s earnings faster than their cost base, leading to high ROCE in the future

Conclusion

2025 was a weird year for investors. The “hottest” assets were gold, bitcoin, and AI hyperscalers, all of which I do not own, as I either don’t understand their value-add or can’t predict their future trajectory. Instead, I own a relatively boring set of high-quality, value-adding businesses that provide a “win-win-win” proposition for customers, employees, and shareholders. In my view, this is the key to generate an above-average rate of return over a wide range of macro scenarios without the need for constant intervention.

My biggest regret last year was not spending sufficient time on equity research and publishing. My “to-do” list of companies to research is growing at an alarming pace!

Thank you for reading and let me know what you would like to read about in 2026!

Sharad, loved your insights of your portfolio, thanks for sharing. Do you by any chance follow Mohnish Prabai? I see few common stocks.

I am also an equity investor in Indian businesses for 6+ years and run a concentrated portfolio of Edelweiss Financial, Vaibhav global and one SBI Small cap fund (weekly SIP). Im excited about the opportunities which we will have in next five seven years in India. Thanks for inspiring, i would love to share my portfolio performance similar to yours over long term.

You are underperforming in International marker and outperforming in Indian market, why not just invest in Indian market. Why even go for International market? Are you not finding enough opportunities in indian market?