Fairfax India Holdings - looking for the shareholders' yachts

Are the exorbitant "2 & 20" management fees worth paying to own some of India's best assets?

Summary

Fairfax India, a "value investing" vessel, has been navigating the challenging yet lucrative Indian market since 2014, captained by Prem Watsa. While the company has accumulated a great set of Indian assets in the decade since inception, its share price performance can only be described as 'subpar', leaving investors wondering: “Where are the shareholders' yachts”. With Prem Watsa’s son Ben set to take the helm in July 2024, it might be a good time to look under the hood at Fairfax India, in order to find out whether the tsunami of management fees would drown future shareholder returns.

A deep-dive (pun intended) follows, covering:

The good: a long track record, conservatively valued assets and share buybacks

The bad: past controversies and share price performance

The ugly: the exorbitant fee structure & potential risks

Valuation: the discount to book is mainly due to the fee structure

Summary: two and twenty does not work

The good

Fairfax India was founded in 2014 by the billionaire investor Prem Watsa and its common shares are listed on the Toronto Stock Exchange under the symbol “FIH.U”. There are many things to like about the company.

The track record:

Prem Watsa has a long record of integrity and fiduciary responsibility since founding Fairfax Financial in 1987

Fairfax India’s book value per share in US$ terms has grown 9.2% annually in the decade since inception, compared to the S&P BSE Sensex 30 which grew book value at 7.1% (measured in US$ terms)

Ben Watsa, who will replace Prem Watsa in July 2024, is pretty accomplished as well. He has twenty-three years of experience in the investment industry and has been running his own India-focused fund since 2017. We hope that Ben and the new board members will re-think the fee structure to more closely align with shareholder interests.

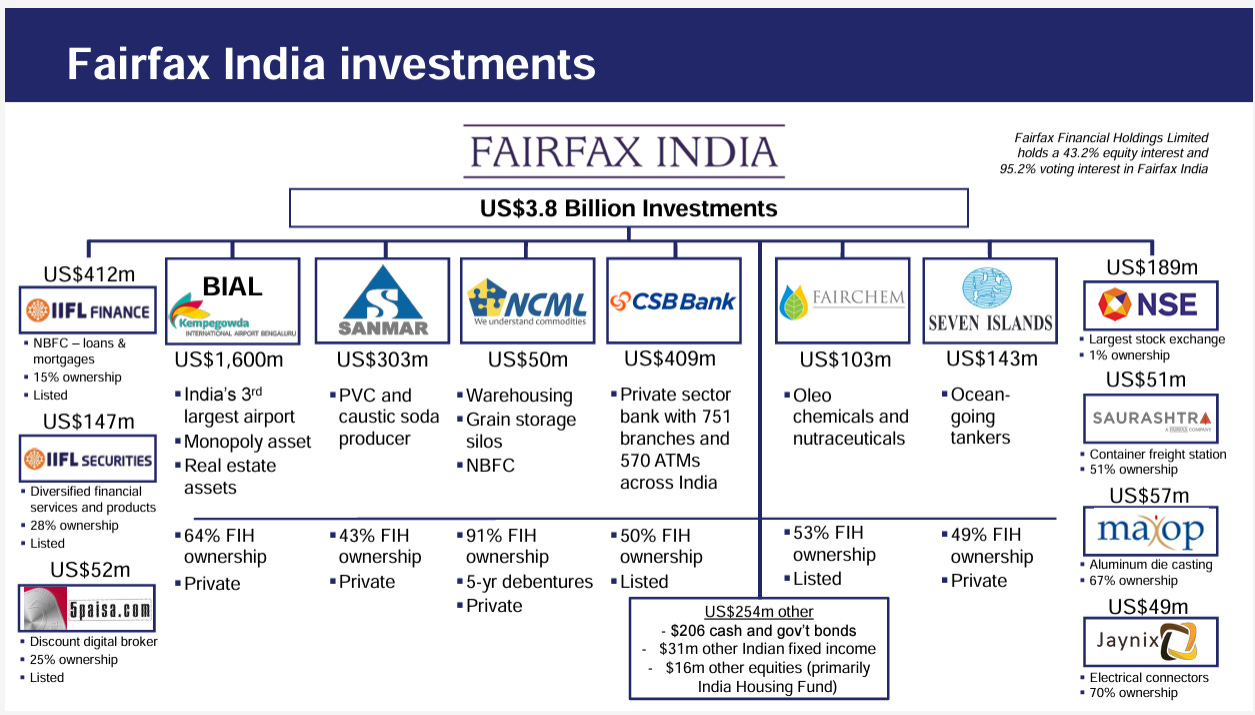

The quality of assets:

Fairax’s ownership of Bangalore Intl. Airport (BIAL) makes up 44% of book value and ~64% of current enterprise value;

Fairax’s values its BIAL stake at $1.6B, which translates to a $2.5B valuation for the entire airport. This seems highly conservative, as they are planning an IPO for the airport with a reported value of $3.7B.

Bangalore Airport is the third busiest airport in India, with their concession valid until 2068 - so it has a long runway ahead (pun intended)

Fairfax expects “normalized” free cash flow to be $260M once the new Terminal is fully operational, valuing the airport at 9.5x FCF; Airports, like BIAL, hold a monopoly on access to a city plus exclusive rights to duty free and dining. Their clientele of travelers usually have very high disposable incomes. So, a typical airport is valued at much higher multiples in the range of 15~20x.

There are talks about a 2nd airport in Bangalore after 2033, but no concrete plans as of yet. Even if this comes up, BIAL would service most of the Bangalore bound passenger and cargo traffic for the next few decades.

There is an additional 460 acres of land adjoining the airport that is being developed, which are not yet factored into the above valuation.

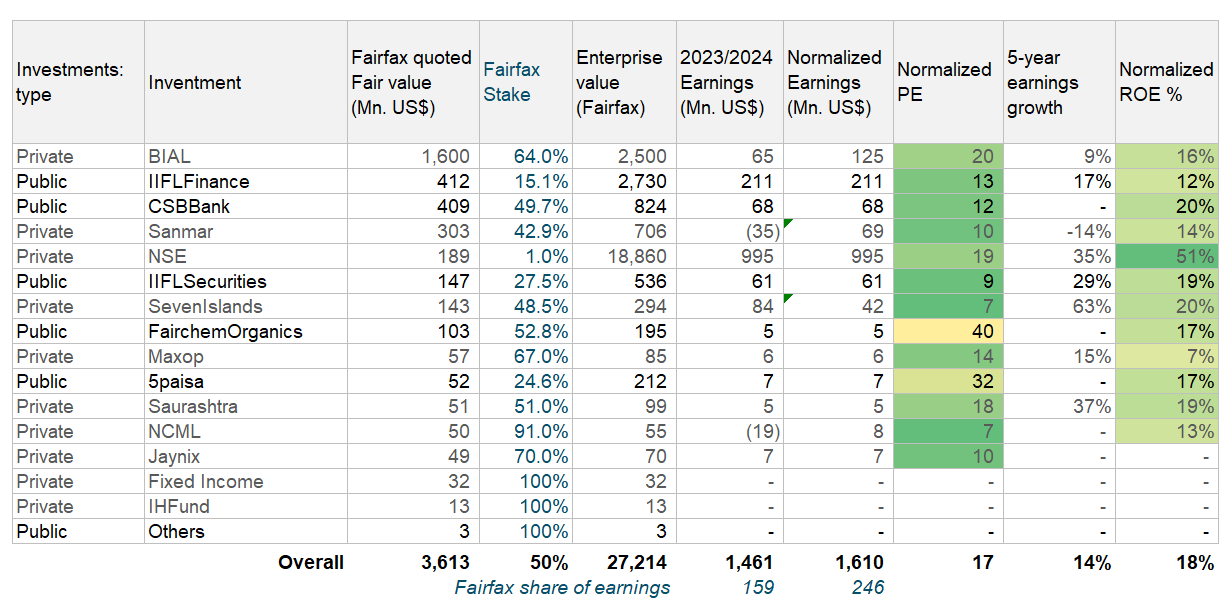

Apart from BIAL, Fairfax owns other quality Indian assets across finance, industrials and logistics (listed below);

The publicly listed portion is mainly in IIFL group and CSB Bank, valued at ~$1.13B (13.2x earnings);

IIFL is one of the larger non-bank finance companies in India. It provides home loans, personal loans, business loans, offers wealth management products and also securities brokerage. RBI (Reserve Bank of India) cited “material supervisory concerns” at IIFL finance’s gold loan division (30% of their IIFL’s business) earlier this year. However, the RBI audit has been completed, and IIFL seems to be rectifying the issues.

CSB is one of the oldest private banks in India, with significant presence in the Southern states. It had a long period of underperformance and losses prior to 2018, when Fairfax acquired a 50% stake. It has since had a spectacular turnaround and is now highly profitable and growing, with plans to have a pan-India presence.

The private portion (excl. BIAL) is valued at $0.89B;

Sanmar, which makes up 34% of this amount, operates in cyclical industries (PVC and Caustic Soda). It broke even in 2022 and made minor losses in 2023.

NSE (India’s largest stock exchange) is the next biggest, at 21%. Fairfax expects to exit this investment in 2024, as they feel it is “fully valued” at current prices

Seven Islands shipping is the third largest holding, making up 16% of the private portion (excl. BIAL); It seems to be very conservatively valued at 3.5x PE and and 3.9x price to free cash flow.

Their investment in NCML (National Commodities Management Services) appears to be underperforming, with the company making major losses. Their initial investment of $159M has been written down to $50M at the end of 2023

Fairfax’s estimates of asset value:

Unlocking value through public listings

Fairfax is is exploring the listing of its larger portfolio companies. This should provide further transparency into the fund's underlying value.

37% of their portfolio is publicly listed; If BIAL’s IPO proceeds as planned, this number will increase to ~80%

Strong balance sheet: $0.5Bn in borrowings compared to ~$3Bn+ in equity

Skin in the game: Fairfax Financial (Prem Watsa’s primary holding company) is Fairfax India’s largest shareholder, with 95% voting interest and 43% economic interest

Fairax India has been aggressively buying back shares since 2020, when the share dropped below book value

Since inception, they have bought back 22.0 million shares (~14% of total free float) for $285 million, or $12.93 per share

The bad

Prem Watsa has had his share of controversies in the past, notably:

A Quebec Superior Court judgment in 2019 found that Watsa and Fairfax acted in a "reprehensible" manner in the acquisition of Fibrek Inc. The court determined that they enabled the acquisition at the "lowest possible price" to the detriment of minority shareholders

There were concerns raised about potential conflicts of interest in Watsa's role on BlackBerry's board, particularly his influence over director nominations and compensation.

Muddy Waters Research went short on Faifax Holdings in Feb 2024, claiming “Fairfax has consistently manipulated asset values and income by engaging in often value destructive transactions to produce accounting gains. We believe a conservative adjustment to book value should be ~-$4.5 billion or ~-18% lower than reported. We see Fairfax as far more akin to GE than to Berkshire Hathaway.” Many of Muddy Waters’ claims have been disputed, and the FFH share price has recovered after a short dip in Feb 2024 following the report. Overall, I don’t see much cause for concern.

Fairfax India’s stock has not kept up with book value since 2020, with price-to-book dropping from ~1x to ~0.7x since the pandemic started. An investor in Fairfax India would be sitting on zero returns since 2017, while the S&P500 & Indian indices have more than doubled in the same 6 year period.

The ugly

The main reason that the stock has underperformed is due to the exorbitant “2&20” management fee structure

Investment and Advisory Fee (I&A Fee): Fairfax Financial provides administration and investment advisory services to Fairfax India and its subsidiaries for an I&A Fee – 1.5% on deployed capital and 0.5% on undeployed capital

Performance Fee: Fairfax India pays a performance fee, calculated at the end of each three-year period, of 20% of any increase (including distributions) in book value per share above a non-compounded 5% increase each year from inception in 2015

Investors in the past have questioned why the fees are linked to book value (which is determined by the management) as opposed to share price, which is more aligned with shareholders. However, once a majority of the portfolio becomes publicly listed, part of this conflict should be resolved, as the underlying asset value will be mostly market-determined.

Risks

Fairfax capital allocation

Misstated asset valuations, particularly within the private portfolio, pose a potential risk. Note: the performance fee is related to book value, so the management has incentives to inflate book value (although I didn’t see any evidence of this happening so far)

Overpaying for future investments or acquiring struggling companies with limited turnaround prospects (similiar to NCML)

Subsidiaries

Further regulatory / supervisory issues at IIFL

Increasing losses / asset write-offs at Sanmar

Litigation related to BIAL or other financial / infrastructure assets

Changes in Indian government policy affecting BIAL and the financial entities

Conflicts of interested between Fairfax Financial and Fairfax India: Fairfax Financial (the Canadian holding company) also owns Indian companies and assets and has continued to purchase Indian assets since 2014

Indian market growth slows down or enters a “stagflation”

Indian rupee deprecation vs. USD (as Fairfax India reports performance in USD terms)

Valuation & potential returns for minority shareholders

Fairfax India's portfolio outperformed the Indian GDP over the past decade. The portfolio achieved a CAGR of 9%, compared to the national GDP's CAGR of 7% (in US$ terms). Fairfax is also situated in some of the fastest growing parts of the economy: finance , infrastructure and industrials. So, I expect the trend of outperformance to continue over the next few decades as well. Based on the estimates below, the portfolio seems conservatively valued currently.

To accurately reflect the performance fee, I used a DCF with various growth scenarios to estimate value/share. Details can be found here.

As you can see the, the discounted asset value is between $2.6 billion and $4.6 billion, which accurately reflects the quality of the assets. However, the discounted value of the fees is substantial at $0.6 billion to $2.0 billion. The upside is limited, since higher growth would translate into higher performance fees. This could be especially worrisome for the upcoming BIAL public listing, which could potentially double the book value per share in one to two years, leading to a windfall performance fee payout.

In contrast, a fixed fee would dramatically improve the valuation - for example:

A fixed fee of $10M~$20M translates to a discounted value of just $83~$166M (assuming the same discount rate of 12%), which could increase the underlying value of Fairax India by a billion $ or more!

Even if we apply a 5% growth to the fixed fee of $10M~$20M to account for inflation, it would still translate only to $150~$200M

I would go further to argue that changing to a fixed fee is also in the best interest of Fairfax Financial (the majority shareholder). I think the market will appreciate the shareholder friendly move and the price to book discount would close, leading to a 33%+ share price increase or $514M in additional market cap. That translates to a gain of $224M for Fairfax Financial, who own 43% of the economic interest of Fairfax India holdings.

Conclusion

Re-surfacing after the deep-dive, it seems the only yacht in sight belongs to management. The Fairfax leadership seem to be “having their cake and eating it too”, with the market correctly valuing the huge fee burden to minority shareholders. We hope the new management team finds a moral compass on board and moves to a more shareholder friendly management structure in the future.

As you are aware, Warren Buffett has produced a stellar investment performance over the past 45 years, compounding returns at 20.46% pa. If you had invested $1,000 in the shares of Berkshire Hathaway when Buffett began running it in 1965, by the end of 2009 your investment would have been worth $4.3m. That's because Buffett runs Berkshire Hathaway as a company in which he co-invests alongside his investors.

If Buffett had set it up as a hedge fund and charged 2% of the value of the funds as an annual fee, plus 20% of any gains, of that $4.3m, $4.0m would belong to him as manager and only $300,000 would belong to you, the investor. And this is the result you would get if your hedge fund manager had equaled Warren Buffett's performance.

Conclusion: Two and twenty does not work.

Sources

Value Investors Club write-ups:

Fairfax India presentation from MOI global “Best Ideas 2022”

Disclaimer: The information contained in this publication is not intended to constitute individual investment advice and is not designed to meet your personal financial situation. The opinions expressed in such publications are those of the publisher and are subject to change without notice. I may from time to time have positions in the securities covered in the articles on this website. I use company declarations and open source information sources believed to be reliable, but their accuracy cannot be guaranteed. The author, shall in no event be held liable to any party for any direct, indirect, punitive, special, incidental, or consequential damages arising directly or indirectly from the use of any of this material.

Appendix

I just finished Fred Schwed Jr.'s hilarious “Where Are the Customers' Yachts?”. It exposes the misalignment between Wall Street and regular investors.

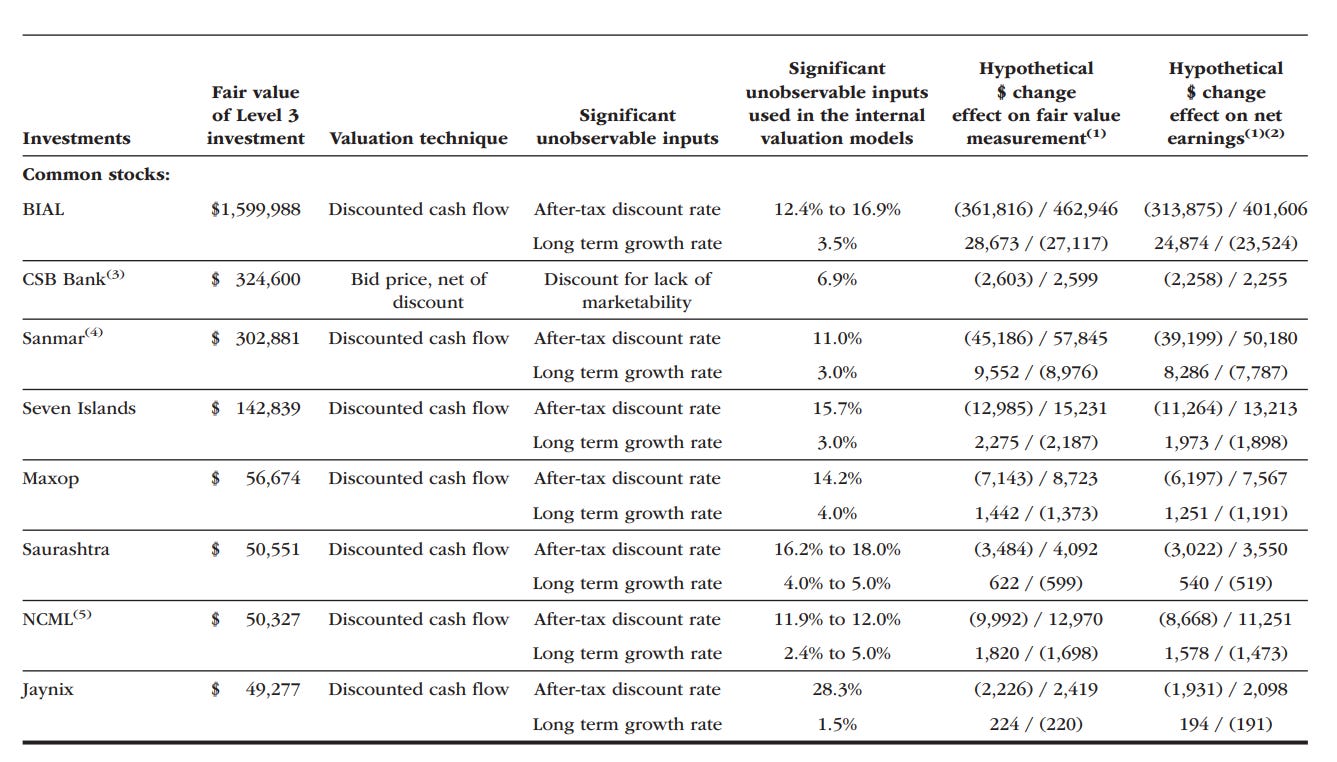

Fairfax’s asset valuation methodology from their 2023 annual report is in the following table.

Great post! Love the analysis. An easier method to get liquidity from this vehicle would be to use dividends as management already owns 44% of FIH right? So from $250M of normalized earning they could pull some out and make it a dividend play. Basically anything except a 2-20 tax on investor. It is a bad idea when you run with other people's capital but insane when you already own 43% of it.

what's a more reasonable fee structure do you think to be able to use the Fairfax name and lean on their balance sheet/cost of capital? 50m/yr off of a ~4bn book they are managing doesn't seem outrageous. Agree that it causes a drag but seems like there's some benefit there too unless I'm missing something.